The post Absorption Costing | Variable Costing | Exam Based Q&A | Brief | Descriptive | Analytical appeared first on EP Online Study.

]]>

Absorption Costing and Variable Costing Exam Based Questions and Answers

It includes Brief Question, Descriptive Questions and Analytical Questions with answers in details

Absorption Costing | External Costing | Traditional Costing

Absorption costing is a traditional costing system.

It is also called full absorption, conventional costing or traditional costing and external costing.

It includes variable cost and fixed cost manufacturing.

Absorption costing includes direct materials, direct labour, variable manufacturing cost and fixed manufacturing cost in product cost.

It includes administrative cost, selling and distribution cost in period cost.

But it does not include fixed manufacturing cost in period cost.

The main object of the business company is to earn more and more profit.

Success or failure of the company is depended on profit.

The income statement measures profit or loss of the company.

There are two types of methods to find out profit and loss from income statement.

Absorption costing and variable costing are two methods to prepare income statement.

Absorption costing is suitable for internal as well as external users but variable costing is suitable for internal users with management decision.

Direct materials, direct labour, variable manufacturing cost and fixed manufacturing cost = Production units × Cost per unit

Period cost under absorption costing = Administrative cost + Selling and distribution cost

Total variable, selling and distribution cost = Sales units × Cost per unit

Income Statement under Absorption Costing

For ….. units

|

Particulars |

Amount |

||

|

Sales Revenue (sales units @ $) |

xxxx |

||

|

(A) |

xxxx |

||

|

Manufacturing cost: |

|

||

|

|

Direct materials (production units @ $) |

|

|

|

|

Direct labour (production units @ $) |

|

|

|

|

Variable production overhead (production units @ $) |

|

|

|

|

Fixed production cost (production units @ $*) |

|

|

|

|

Total manufacturing cost or Cost of production |

xxxx |

|

|

Add: |

Beginning inventory (opening stock @ $) |

xxxx |

|

|

Less: |

Ending inventory (closing stock @ $) |

(xxx) |

|

|

|

COGS before adjustment |

xxxx |

|

|

Add: |

Under absorption# manufacturing cost (compare with actual) |

xxxx |

|

|

Less: |

Over absorption manufacturing cost (compare with actual) |

(xxx) |

|

|

|

COGS after adjustment (B) |

xxxx |

|

|

|

Gross profit (A–B) |

xxxx |

|

|

Less: |

Variable administrative cost (production units x $) |

xxxx |

|

|

|

Variable S&D cost (sales units x $) |

xxxx |

|

|

Less: |

Fixed administrative cost (production units x $) |

xxxx |

|

|

|

Fixed S & D cost (sales units x $) |

xxxx |

xxxx |

|

Net Income |

$xxxx |

||

Fixed cost per unit (FCPU*) = Fixed manufacturing cost ÷ Normal output

Either over absorption# or under absorption

Variable Costing | Internal Costing | Direct Costing

Variable costing is also known as internal costing, direct costing and marginal costing.

Variable cost helps to administrator to solve the problem about production planning.

Under this method, production cost is calculated on variable basis.

Variable costing includes direct materials, direct labour and variable manufacturing cost in product cost.

It includes fixed manufacturing cost, administrative, selling and distribution cost in period cost.

Direct materials, direct labour, variable manufacturing cost:

= Production units x Cost per unit

Period costing under variable costing = Fixed manufacturing cost + Administrative cost + S&D cost

Total variable, selling and distribution cost = Sales units × Cost per unit

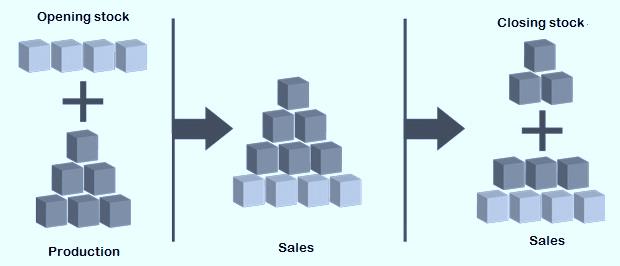

Sold units = Opening stock + Production – Closing stock

Income Statement under Variable Costing

|

Particulars |

Amount $ |

|||

|

Sales revenue (sales units @ $) |

xxxx |

|||

|

(A) |

xxxx |

|||

|

Variable cost: |

|

|||

|

|

Direct materials |

(production units @ $) |

xxxx |

|

|

|

Direct labour |

(production units @ $) |

xxxx |

|

|

|

Variable production overhead |

(production units @ $) |

xxxx |

|

|

|

|

Total variable cost or Cost of production |

xxxx |

|

|

Add: |

Beginning inventory |

(opening stock @ $) |

xxxx |

|

|

Less: |

Ending inventory |

(closing stock @ $) |

xxxx |

|

|

|

|

COGS (B) |

xxxx |

|

|

|

|

Gross contribution (A – B) |

xxxx |

|

|

Less: |

Variable administrative cost |

(production units x $) |

xxxx |

|

|

Less: |

Variable S&D cost |

(sales units x $) |

xxxx |

|

|

|

|

Net contribution |

xxxx |

|

|

Less: |

Fixed production cost |

( ± absorption, if any) |

xxxx |

|

|

Fixed administrative cost |

(production units x $) |

xxxx |

|

|

|

Fixed S&D cost |

(sales units x $) |

xxxx |

|

|

|

Net Income |

$xxxx |

|||

Note: If there is under absorption in absorption costing, it is added with fixed manufacturing cost in variable costing

If there is over absorption in absorption costing, it is deducted from fixed manufacturing cost in variable costing

Reconciliation of Difference in Net Cost

If there is no difference in the size of opening stock and closing stock, in such a condition net income of absorption costing and variance costing is same.

The difference between opening stock, closing stock and fixed manufacturing overhead are the main cause of difference in net income.

These differences can be solved by reconciliation.

Where:

|

Difference in stock units |

= Difference in income ÷ Fixed cost per unit |

|

According to variable costing, Opening stock in units |

= Closing stock in units − Difference in stock units |

|

According to absorption costing, Opening stock in units |

= Closing stock in units + Difference in stock units |

|

|

|

|

According to variable costing, Closing stock– Opening stock |

= Difference |

|

According to absorption costing, Opening stock – Closing stock |

= Difference |

Reconciliation Statement

|

Particulars |

Amount |

|

Net income as per variable costing |

xxxx |

|

Add: Closing stock (units @ FCPU) |

xxxx |

|

Less: Opening stock (units @ FCPU) |

(xxx) |

|

Net income as per absorption costing |

xxxx |

Or

Reconciliation Statement

|

Particulars |

Amount |

|

Net income as per absorption costing |

xxxx |

|

Add: Opening stock (units @ FCPU) |

xxxx |

|

Less: Closing stock (units @ FCPU) |

(xxx) |

|

Net income as per variable costing |

xxxx |

Click on the photo for FREE eBooks

Brief Questions

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 1

The extracted data are given to you:

Opening stock 10,000 units

Sales 60,000 units

Closing stock 20,000 units

Required: Production units

[Answer: 70,000 units]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 2

The extracted data are given to you:

Production 20,000 units

Sales 25,000 units

Required: Stock

[Answer: Opening stock = 5,000 units]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 3

The extracted data are taken from ABC Manufactures Company:

Sales units 9,000 units

Production units 12,000 units

Cost data:

Direct materials 60

Direct labor 40

Variable factory overheads 30

Fixed manufacturing overheads $180,000

Required: Cost of production under variable costing

[Answer: COP = $15,60,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 4

The extracted data are taken from BC Manufactures Company:

Production units 12,000 units

Normal output 9,000 units

Cost data:

Direct materials 60

Direct labor 40

Variable factory overheads 30

Fixed manufacturing overheads $180,000

Required: Cost of production under absorption costing

[Answer: COP = $18,00,000] * FCPU or SFOR = $20

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 5

ABC Manufacturing Company has following extracted data:

Normal output 35,000 units

Production 30,000 units

Opening stock 5,000 units

Closing stock 10,000 units

Cost data per unit:

Direct materials $260,000

Direct labour $350,000

Variable factory overheads $275,000

Factory manufacturing overheads $200,000

Required: Cost of goods sold under variable costing

[Answer: COGS = $735,500]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 6

ABC Manufacturing Company has following extracted data:

Standard fixed overhead rate (SFOR) $7

Production 30,000 units

Sales 35,000 units

Opening stock 10,000 units

Cost data per unit:

Direct materials $260,000

Direct labour $350,000

Variable factory overheads $275,000

Required: Cost of goods sold under absorption costing

[Answer: COGS = $12,77,500] *Closing stock = 5,000 units

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 7

The following extracted information is available:

Net income as per absorption costing $450,000

Opening stock 10,000 units

Closing stock 20,000 units

Normal output was 40,000 units

Fixed manufacturing cost $200,000

Required: Reconciliation statement

[Answer: Net profit as per variable costing = $400,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 8

The following extracted information is available:

Net income as per variable costing $450,000

Opening stock 10,000 units

Closing stock 20,000 units

Normal output was 40,000 units

Fixed manufacturing cost $200,000

Required: Reconciliation statement

[Answer: Net profit as per absorption costing = $500,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 9

Following extracted information is given to you:

Cost of goods sold before adjustment $500,000

Fixed manufacturing cost $125,000

Normal output 25,000 units

Output for the period 30,000 units

Required: Cost of goods sold after adjustment

[Answer: $475,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 10

Following extracted information is given to you:

Cost of goods sold before adjustment $500,000

Fixed manufacturing cost $125,000

Normal output 25,000 units

Output for the period 22,000 units

Required: Cost of goods sold after adjustment

[Answer: $515,000]

######

|

Click on the link for YouTube videos |

|

|

Accounting Equation |

|

|

Journal Entries in Nepali |

|

|

Journal Entries |

|

|

Journal Entry and Ledger |

|

|

Ledger |

|

|

Subsidiary Book |

|

|

Cashbook |

|

|

Trial Balance and Adjusted Trial Balance |

|

|

Bank Reconciliation Statement (BRS) |

|

|

Depreciation |

|

|

|

|

|

Click on the link for YouTube videos chapter wise |

|

|

Financial Accounting and Analysis (All videos) |

|

|

Accounting Process |

|

|

Accounting for Long Lived Assets |

|

|

Analysis of Financial Statement |

|

######

Descriptive Questions

VARIABLE COSTING

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 1

Following are data pertaining to month of December of operation for ABC Textile Company related to school dress:

|

Opening stock 2,000 units |

Administrative expenses: |

|

Units produced 6,000 units |

Fixed $250,000 |

|

Normal output 5,000 units |

Variable $250,000 |

|

Units sold 7,000 units |

|

|

Selling price per unit $300 |

Selling and distribution expenses: |

|

Fixed manufacturing cost $200,000 |

Variable (per unit) $20 |

|

Variable cost per unit: |

Fixed (per unit) $15 |

|

Direct materials 50 |

|

|

Direct labor 40 |

|

|

Factory overheads 30 |

|

Required: (a) Income statement under variable costing; (b) Reconciliation statement

[Answer :(1) Net income = $315,000; (2) $275,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 2

AK Manufacturing Company has reported its income statement under absorption costing technique as under:

|

Particulars |

Amount |

Amount |

|

|

Sales revenue (10,000 units x $45) |

|

450,000 |

|

|

Less: |

Cost of goods sold: |

|

|

|

|

Beginning inventory (2,000 x $27) |

54,000 |

|

|

|

Variable cost (9,000 x $23) |

207,000 |

|

|

|

Fixed mfg. cost (9,000 x $4) |

36,000 |

|

|

|

Ending inventory (1,000 x $27) |

(27,000) |

(270,000) |

|

|

Gross margin before adjustment |

|

180,000 |

|

Less: |

Fixed manufacturing cost under absorbed |

|

4,000 |

|

|

Gross margin after adjustment |

|

176,000 |

|

Less: |

Other variable cost |

|

50,000 |

|

Net income before tax |

|

$126,000 |

|

Required: Income statement under variable costing technique

[Answer: Net income under variable costing = $130,000;

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 3

Following extracted details are given to you by EP Industries:

Normal capacity 200,000 units per year

Standard variable manufacturing expenses $20 per unit

Fixed manufacturing overhead $300,000 per year

Variable selling expenses $2 per unit

Fixed selling expenses $100,000

Unit sale price $25

The operating results for the year ending December of the last year were as follows

Sales 150,000 units

Production 180,000 units

Required: (a) variable costing income statement; (b) Reconciled profit under absorption costing

[Answers: Income under VC = $50,000, under AC = $95,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 4

XYZ Manufacturing Company with normal capacity of 50,000 units supplied you with the following particular:

|

Production |

55,000 units |

|

Sale |

60,000 units |

|

Closing stock |

5,000 units |

|

Unit variable manufacturing cost |

$6 |

|

Unit fixed manufacturing overhead |

$3 |

|

Unit variable selling and administrative cost |

$2 |

|

Fixed selling & administrative cost |

$90,000 |

|

Unit selling price |

$15 |

Required: (1) Variable costing income statement; (2) Reconciled profit under absorption costing

[Answers: (1) $180,000; (2) $165,000]

ABSORPTION COSTING

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 5

The extracted cost abstract of EP Manufacturing Company was as follows:

|

Particulars |

Units cost |

The operations of the year ended December 2021 were: |

|

|

Direct materials |

$12 |

Opening stock |

10,000 units |

|

Direct labour |

$3 |

Production |

90,000 units |

|

Variable manufacturing cost |

$2 |

Sales |

80,000 units |

|

Variable selling & distribution expenses |

$1 |

Sales price per unit |

$30 |

Budgeted normal output was 100,000 units with $200,000 fixed manufacturing cost. The fixed selling and distribution expenses were $50,000

Required: (1) Income statement under absorption costing; (2) Reconciled profit under variable costing

[Answer: Net profit: A.C = $730,000; V.C = $710,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 6

The summarized data of AM Manufacturing Concern for a capacity output of 50,000 units for a year is reported as:

|

Items |

Units Cost |

Items |

Units Cost |

|

Direct materials |

$14 |

Fixed manufacturing overhead |

$75,000 annual |

|

Direct labour |

$6 |

Fixed selling expenses |

$50,000 annual |

|

Variable manufacturing overhead |

$4 |

Production |

45,000 units |

|

Variable selling expenses |

$2 |

Sales |

40,000 units |

|

Sales price per unit |

$30 |

|

|

Required: (1) Absorption costing income statement; (2) Reconciled profit under variable costing

[Answers: (1) Net income = $42,500; (2) $35,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 7

ABC Manufacturing Company with normal capacity of 20,000 units furnished you the following information:

|

Beginning inventory units |

3,000 |

Standard variable cost |

$6.50 |

|

Units produced during the year |

18,000 |

Fixed factory overhead at normal capacity |

$50,000 |

|

Units sold during the year |

20,000 |

Fixed selling and distribution cost |

$5,000 |

|

|

|

Unit selling price |

$12 |

Required: (1) Income statement under absorption costing; (2) Reconciled profit under variable costing

[Answers: (1) $50,000; (2) $55,000] *Under absorption = $5,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 8

Following are the references data of month June of operation for XYZ Company:

|

Opening stock |

15,000 units |

Variable cost: |

|

|

Units produced |

45,000 units |

Direct materials per unit |

$4 |

|

Units sold |

50,000 units |

Direct labour per unit |

$2 |

|

Normal output |

50,000 units |

Factory overheads per unit |

$1 |

|

Selling price per unit |

$20 |

Administrative |

$50,000 |

|

Fixed manufacturing cost |

$150,000 |

Selling and distribution per unit |

$1 |

|

|

|

Fixed cost: |

|

|

|

|

Manufacturing |

$150,000 |

|

|

|

Administrative |

$40,000 |

|

|

|

Selling and distribution |

$30,000 |

Required: (1) Income statement under absorption costing; (2) Reconciliation statement

[Answer: (1) Net income = $315,000; (2) $330,000]

ABSORPTION AND VARIABLE COSTING

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 9

Max Company uses direct costing for internal control purchase and absorption costing for external reporting purpose. The following differences are located while comparing the two statements.

|

Items |

Variable Costing |

Absorption Costing |

|

|

Variable manufacturing cost |

$60,000 |

$60,000 |

|

|

Fixed manufacturing cost charged |

$25,000 |

$30,000 |

|

|

Fixed selling and administrative cost |

$40,000 |

$40,000 |

|

|

Variable selling cost per unit |

$2 |

$2 |

|

|

Selling price per unit |

$30 |

$30 |

|

Management also projected the following data for the inventory:

|

Beginning inventory units 1,000 |

Sales units 5,000 |

|

Production units 6,000 |

Closing stock units 2,000 |

Cost of beginning inventory is the same as the cost of production in the period.

Required: Income statement by using absorption costing and variable costing approach

[Answers: Net profit = $30,000; $25,000]

*Over absorption $5,000]

Click on the photo for FREE eBooks

Analytical Questions

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 1

Fame Readymade Garment has given following data at the end of December 2020; it was anticipated that sales would rise 20% in year 2021. Therefore, production was increased from 20,000 units to meet this expected demand.

|

Particulars |

Amount |

|

Sales units during year |

20,000 |

|

Selling price per unit |

300 |

|

Direct materials |

45 |

|

Direct labors |

75 |

|

Variable manufacturing overheads |

30 |

|

Variable administrative expenses |

2,50,000 |

|

Variable selling and distribution expenses |

1,00,000 |

|

Fixed manufacturing cost for the year |

9,60,000 |

|

Fixed administrative cost |

6,00,000 |

|

Fixed selling and distribution cost |

4,00,000 |

All taxes are to be ignored. The beginning inventory of the year was nil.

You are required to prepare profit statement for the year ending December 2021

(1) Net income as per variable costing; (2) Net income as per absorption costing

[Answer: (1) V.C. = $690,000 (2) A.C. = $10,90,000;

* Over absorption = $240,000; Production = 24,000 units]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 2

XYZ Ltd uses direct costing for internal control purposes and absorption costing for external reporting purposes. The company uses the following unit costs for the one product it manufactures:

|

Projected cost per unit: |

|

|

Direct materials |

$60 |

|

Direct labour |

$38 |

|

Variable manufacturing |

$12 |

|

Fixed manufacturing cost |

$10 (Based on 10,000 units per month) |

|

Variable selling and administrative cost |

$8 |

|

Fixed selling and administrative cost |

$5.60 (Based on 10,000 units per month) |

The projected selling price is $160 per unit. The fixed costs remain fixed within the relevant range of 4,000 to 16,000 units of production.

Management has also projected the following data for the month:

Opening stock 2,000 units

Production 9,000 units

Sales 7,500 units

Required: projected income statement under direct costing and absorption costing.

[Answer: Variable costing: $1,59,000, Absorption costing: $1,74,000;

* Under absorption cost =100,000 – 90,000 = 10,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 3

ABC Manufacturing Company has following data:

Income Statement under Absorption Costing

[For 14,000 units]

|

Particulars |

Amount |

|||

|

Sales |

[16,000 @ $80] [A] |

12,80,000 |

||

|

Manufacturing of goods sold: |

|

|

||

|

|

Direct materials |

[14,000 units @ $20] |

280,000 |

|

|

|

Direct labour |

[14,000 units @ $10] |

140,000 |

|

|

|

Variable production cost |

[14,000 units @ $15] |

210,000 |

|

|

|

Fixed manufacturing cost |

[14,000 units @ $5] |

70,000 |

|

|

|

|

Manufacturing cost @ $50] |

700,000 |

|

|

Add: |

Opening stock |

[3,000 units @ $50] |

150,000 |

|

|

Less: |

Closing Stock |

[1,000 units @ $50] |

(50,000) |

|

|

|

|

COGS before adjustment |

800,000 |

|

|

Add: |

Under absorption of fixed mfg cost |

|

50,000 |

|

|

|

|

COGS after adjustment (B) |

850,000 |

|

|

|

|

Gross profit [A –B] |

430,000 |

|

|

Less: |

Administrative and selling cost: |

|

|

|

|

|

Fixed |

|

80,000 |

|

|

|

Variable |

|

50,000 |

130,000 |

|

Net income |

300,000 |

|||

Required: (a) Income statement under variable costing;

(b) Reconciliation of profit between absorption costing and variable costing.

[Answer: Net income under V.C. = $3,10,000;

* Fixed Manufacturing cost in V.C = $120,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 4

MS Tech (P) Ltd produces and assembles computer components. The following internal data is available:

Income Statement under Variable Costing

For 20,000 units

|

Particulars |

Amount |

|||

|

Sales revenue |

[21,000 units @ $100] |

21,00,000 |

||

|

(A) |

21,00,000 |

|||

|

Variable cost: |

|

|

||

|

|

Direct materials |

[20,000 units @ $30] |

6,00,000 |

|

|

|

Direct labour |

[20,000 units @ $15] |

3,00,000 |

|

|

|

Variable manufacturing cost |

[20,000 units @ $10] |

2,00,000 |

|

|

|

Cost of production @ $55) |

11,00,000 |

||

|

Add: |

Beginning inventory |

[2,000 units @ $55] |

1,10,000 |

|

|

Less: |

Ending Inventory |

[1,000 units @ $55] |

55,000 |

|

|

|

COGS (B) |

11,55,000 |

||

|

|

Gross contribution (A – B) |

9,45,000 |

||

|

Less: |

Variable selling administrative cost |

|

1,05,000 |

|

|

|

Net contribution |

8,40,000 |

||

|

Less: |

Fixed manufacturing cost |

|

420,000 |

|

|

|

Fixed selling and administrative cost |

|

+ 350,000 |

7,70,000 |

|

Net income |

70,000 |

|||

Normal capacity for the period is 20,000 units.

Required: (1) Net income under external period; (2) Reconciliation statement for the period

[Answer: Net income under A.C. = $49,000; * FCPU = $21]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 5

The following information is given by DT Manufacturing Company:

Income Statement under Variable Costing

For 27,000 units

|

Particulars |

Amount |

|||

|

Sales revenue |

[28,000 units @ $30] |

840,000 |

||

|

(A) |

840,000 |

|||

|

Variable cost: |

|

– |

||

|

|

Direct materials |

[27,000 units @ $5] |

135,000 |

|

|

|

Direct labour |

[27,000 units @ $8] |

216,000 |

|

|

|

Variable manufacturing cost |

[27,000 units @ $5] |

135,000 |

|

|

|

Cost of production @ $18) |

486,000 |

||

|

Add: |

Beginning inventory |

[3,000 units @ $18] |

54,000 |

|

|

Less: |

Ending Inventory |

[2,000 units @ $18] |

36,000 |

|

|

|

COGS (B) |

504,000 |

||

|

|

Gross contribution (A – B) |

336,000 |

||

|

Less: |

Variable administrative and selling cost |

|

86,000 |

|

|

|

Net contribution |

250,000 |

||

|

Less: |

Fixed manufacturing cost |

|

100,000 |

|

|

|

Fixed selling and administrative cost |

|

+ 50,000 |

150,000 |

|

Net income |

100,000 |

|||

Normal capacity for the period is 25,000 units.

Required: (1) Conversion the income statement into absorption costing statement; (2) Reconciliation statement

[Answer: (1) $96,000; (2) $100,000;

* Over absorption = $8,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 6

The following information is available from Nepal Polymers (P) Ltd:

|

Particulars |

January |

February |

|

Selling price per unit |

$100 |

$100 |

|

Direct materials and labour per unit |

$25 |

$25 |

|

Variable manufacturing cost per unit |

$15 |

$15 |

|

Variable selling and administrative cost per unit |

$10 |

$10 |

|

Fixed manufacturing cost |

$140,000 |

$140,000 |

|

Fixed selling and administrative cost |

10% of sales |

10% of sales |

|

Units |

January |

February |

|

Production units |

6,000 |

8,000 |

|

Sales units |

5,500 |

7,000 |

Normal output is 7,000 units per month

Required: (1) Income statement under variable costing; (2) Income statement under absorption costing

[Answer: (1) V.C. = $80,000 and $140,000;

(2) A.C. = $90,000 and $160,000;

* Closing stock in Jan = 500 units; Feb = 1,500 units;

*Under absorption in January = $20,000;

Over absorption in February = $20,000

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 7

A manufacturing company provides you the following data for three accounting periods:

Standard capacity is 10,000 units per month. Fixed manufacturing costs budgeted per month $400,000

Production, sales and inventory changes were as follows:

|

Period |

Standard capacity |

Produced units |

Sold units |

|

|

January |

90% |

9,000 |

9,000 |

|

|

February |

110% |

11,000 |

9,000 |

|

|

March |

85% |

8,500 |

10,000 |

|

Standard capacity utilized by 10,000 units

Other information:

|

Administrative and selling expenses were: |

Variable cost per unit was as following: |

|

Variable $20 per unit |

Materials $40 |

|

Fixed selling price per period $300,000 |

Direct labour $40 |

|

|

Manufacturing $20 |

|

|

Selling price per unit $200 |

Determine the income under:

(1) Absorption costing for three months; (2) Marginal costing for three months

(3) Reconciliation of the difference between the net incomes reported under two concepts.

[Answer: (1) $20,000, $100,000, $40,000 (2) $20,000, $20,000, $100,000]

* Absorption: Under in January = $40,000; Over in February = $40,000;

Under in March = $60,000]

EP Online Study

Thank you for investing your time.

Please comment on the article.

You can help us by sharing this post on your social media platform.

Jay Google, Jay YouTube, Jay Social Media

जय गूगल. जय युट्युब, जय सोशल मीडिया

The post Absorption Costing | Variable Costing | Exam Based Q&A | Brief | Descriptive | Analytical appeared first on EP Online Study.

]]>The post Absorption costing | Variable costing | Reconciliation Statement | Problems and solutions appeared first on EP Online Study.

]]>

Absorption Costing | External Costing | Traditional Costing

Absorption costing is a traditional costing system.

It is also called full absorption, conventional costing or traditional costing and external costing.

It includes variable cost and fixed cost manufacturing.

Absorption costing includes direct materials, direct labour, variable manufacturing cost and fixed manufacturing cost in product cost.

It includes administrative cost, selling and distribution cost in period cost.

But it does not include fixed manufacturing cost in period cost.

The main object of the business company is to earn more and more profit.

Success or failure of the company is depended on profit.

The income statement measures profit or loss of the company.

There are two types of methods to find out profit and loss from income statement.

Absorption costing and variable costing are two methods to prepare income statement.

Absorption costing is suitable for internal as well as external users but variable costing is suitable for internal users with management decision.

Direct materials, direct labour, variable manufacturing cost and fixed manufacturing cost = Production units × Cost per unit

Period cost under absorption costing = Administrative cost + Selling and distribution cost

Total variable, selling and distribution cost = Sales units × Cost per unit

Variable Costing | Internal Costing | Direct Costing

Variable costing is also known as internal costing, direct costing and marginal costing.

Variable cost helps to administrator to solve the problem about production planning.

Under this method, production cost is calculated on variable basis.

Variable costing includes direct materials, direct labour and variable manufacturing cost in product cost.

It includes fixed manufacturing cost, administrative, selling and distribution cost in period cost.

Direct materials, direct labour, variable manufacturing cost:

= Production units x Cost per unit

Period costing under variable costing = Fixed manufacturing cost + Administrative cost + S&D cost

Total variable, selling and distribution cost = Sales units × Cost per unit

Sold units = Opening stock + Production – Closing stock

Reconciliation of Difference in Net Cost

If there is no difference in the size of opening stock and closing stock, in such a condition net income of absorption costing and variance costing is same.

The difference between opening stock, closing stock and fixed manufacturing overhead are the main cause of difference in net income.

These differences can be solved by reconciliation.

Where:

|

Difference in stock units |

= Difference in income ÷ Fixed cost per unit |

|

According to variable costing, Opening stock in units |

= Closing stock in units − Difference in stock units |

|

According to absorption costing, Opening stock in units |

= Closing stock in units + Difference in stock units |

|

|

|

|

According to variable costing, Closing stock– Opening stock |

= Difference |

|

According to absorption costing, Opening stock – Closing stock |

= Difference |

Reconciliation Statement

|

Particulars |

Amount |

|

Net income as per variable costing |

xxxx |

|

Add: Closing stock (units @ FCPU) |

xxxx |

|

Less: Opening stock (units @ FCPU) |

(xxx) |

|

Net income as per absorption costing |

xxxx |

Or

Reconciliation Statement

|

Particulars |

Amount |

|

Net income as per absorption costing |

xxxx |

|

Add: Opening stock (units @ FCPU) |

xxxx |

|

Less: Closing stock (units @ FCPU) |

(xxx) |

|

Net income as per variable costing |

xxxx |

Or

Reconciliation Statement

|

Particulars |

Year 1 |

Year 2 |

|

Net income as per variable costing |

xxxx |

xxxx |

|

Net income as per absorption costing |

xxxx |

xxxx |

|

Different in income |

xxxx |

xxxx |

|

Opening stock in units |

xxxx |

xxxx |

|

Closing stock in units |

xxxx |

xxxx |

|

Different stock in units (A) |

xxxx |

xxxx |

|

Fixed cost per unit (B) |

x |

x |

|

Different in income (A x B) |

xxxx |

xxxx |

Keep in Mind (KIM)

|

FMC = fixed manufacturing cost per unit |

|

|

FCPU = fixed cost per unit |

= Fixed manufacturing cost ÷ Normal output |

|

SFOR = standard fixed overhead rate |

|

######

|

Click on the link for YouTube videos |

|

|

Accounting Equation |

|

|

Journal Entries in Nepali |

|

|

Journal Entries |

|

|

Journal Entry and Ledger |

|

|

Ledger |

|

|

Subsidiary Book |

|

|

Cashbook |

|

|

Trial Balance and Adjusted Trial Balance |

|

|

Bank Reconciliation Statement (BRS) |

|

|

Depreciation |

|

|

|

|

|

Click on the link for YouTube videos chapter wise |

|

|

Financial Accounting and Analysis (All videos) |

|

|

Accounting Process |

|

|

Accounting for Long Lived Assets |

|

|

Analysis of Financial Statement |

|

######

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 3A

Nepal Beverages Limited produces mineral water. It sales its product in 10 liter’s pet jar.

The normal annual level of operations is 36,000 units. Data for the last financial years 2020 was as follows:

|

Production |

40,000 units |

|

Sales |

32,000 units |

|

Selling price per units |

$60 |

|

Costs per units: |

|

|

Direct materials |

$14 |

|

Direct labors |

$12 |

|

Variable manufacturing overheads |

$8 |

|

Fixed manufacturing overheads |

$2,16,000 (based on normal output) |

|

Administrative costs: |

|

|

Fixed |

$50,000 |

|

Variable |

5% of sales revenue |

|

Selling and distribution overhead: |

|

|

Fixed |

$30,000 |

|

Variable |

5% of selling price per unit |

There was no opening stock of finished goods and the work-in-progress.

You are required to: (i) Prepare an income statement based on direct costing for the year ended 2021

(ii) Prepare an income statement based on absorption costing for the year ended 2021

(iii) Reconciliation statement

[Answer: (i) $320,000 (ii) $368,000]

SOLUTION:

Given and working note:

|

Sold units |

= |

Opening stock + Production – Closing stock |

|

32,000 |

= |

Nil + 40,000 – Closing stock |

|

Closing stock |

= |

8,000 units |

|

Again, |

|

|

|

Fixed cost per unit [FCPU] |

= |

Factory overhead ÷ Normal output |

|

|

= |

$216,000 ÷ 36,000 units |

|

|

= |

$6 |

Income Statement under Variable Costing

For 40,000 cases

|

Particulars |

|

Amount |

||

|

Sales revenue |

[32,000 units @ $60] |

19,20,000 |

||

|

(A) |

19,20,000 |

|||

|

Variable cost: |

|

|

||

|

|

Direct materials |

[40,000 units @ $12] |

4,80,000 |

|

|

|

Direct labour |

[40,000 units @ $14] |

5,60,000 |

|

|

|

Variable manufacturing cost |

[40,000 units @ $8] |

3,20,000 |

|

|

|

Cost of production @ $34) |

13,60,000 |

||

|

Add: |

Beginning inventory |

[0 units @ $34] |

– |

|

|

Less: |

Ending inventory |

[8,000 units @ $34] |

2,72,000 |

|

|

|

COGS (B) |

10,88,000 |

||

|

|

Gross contribution (A – B) |

8,32,000 |

||

|

Less: |

Variable administrative cost |

[sales @5% = 19,20,000@5%] |

(96,000) |

|

|

Less: |

Variable S&D cost |

[40,000 x 60@5%] |

(1,20,000) |

|

|

|

Net contribution |

6,16,000 |

||

|

Less: |

Fixed manufacturing cost |

[given] |

216,000 |

|

|

|

Fixed administrative cost |

[given] |

50,000 |

|

|

|

Fixed S&D cost |

[given] |

30,000 |

(2,96,000) |

|

Net Income |

$3,20,000 |

|||

Income Statement under Absorption Costing

For 40,000 cases

|

Particulars |

|

Amount |

||

|

Sales revenue |

[32,000 units @ $60] |

19,20,000 |

||

|

(A) |

19,20,000 |

|||

|

Manufacturing cost: |

|

|

||

|

|

Direct materials |

[40,000 units @ $12] |

4,80,000 |

|

|

|

Direct labour |

[40,000 units @ $14] |

5,60,000 |

|

|

|

Variable production cost |

[40,000 units @ $8] |

3,20,000 |

|

|

|

Fixed manufacturing cost |

[40,000 units @ $6] |

2,40,000 |

|

|

|

Cost of production @ 40) |

16,00,000 |

||

|

Add: |

Beginning inventory |

[0 units @ $40] |

Nil |

|

|

Less: |

Ending inventory |

[8,000 units @ $40] |

3,20,000 |

|

|

|

COGS before adjustment |

12,80,000 |

||

|

Add: |

Under absorption |

|

– |

|

|

Less: |

Over absorption |

[$240,000 A.C. – $216,000 V.C.] |

24,000 |

|

|

|

COGS after adjustment (B) |

12,56,000 |

||

|

|

Gross profit (A–B) |

6,64,000 |

||

|

Less: |

Variable administrative cost |

|

96,000 |

|

|

|

Variable S&D cost |

|

120,000 |

|

|

Less: |

Fixed administrative cost |

|

50,000 |

|

|

|

Fixed S&D cost |

|

30,000 |

(2,96,000) |

|

Net Income |

$3,68,000 |

|||

Reconciliation Statement

|

Particulars |

Amount |

|

Net income as per variable cost |

320,000 |

|

Add: Closing stock (8,000 units @ $6) |

48,000 |

|

Less: Opening stock (0 units @ $6) |

Nil |

|

Net income as per absorption cost |

$368,000 |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 3B

ABC Manufacturing Company has following information related to a product:

|

Year |

Production |

Sales |

Sales price per unit |

|

2019 |

170,000 |

140,000 |

$25 |

|

2020 |

140,000 |

160,000 |

$25 |

Other information:

|

Normal production 150,000 units |

Variable cost per unit: |

Administrative and selling cost: |

|

Fixed production cost $750,000 |

Direct materials $5 |

Variable 5% of sales |

|

|

Direct labour $6 |

Fixed $325,000 |

|

|

Production cost $4 |

|

Required: (1) Income statement under variable costing for 2020 and 2021

(2) Income statement under absorption costing for 2020 and 2021;

(3) Reconciliation statement

[Answer: Variable costing 150,000 and 325,000;

Absorption costing 300,000 and 225,000]

SOLUTION:

Given and working note:

|

Sold units |

= |

Opening stock + Production – Closing stock |

|

140,000 |

= |

Nil + 170,000 – Closing stock |

|

Closing stock |

= |

30,000 |

Closing stock of last year becomes opening stock of current year

|

Sold units |

= |

Opening stock + Production – Closing stock |

|

140,000 |

= |

30,000 + 140,000 – Closing stock |

|

Closing stock |

= |

10,000 |

Fixed cost per unit [FCPU]

= Factory overhead old ÷ Normal output

= $750,000 ÷ 150,000 units

= $5

Income Statement under Variable Costing

170,000 and 140,000 units

|

Particulars |

Year 2020 |

Year 2021 |

||

|

Sales revenue |

[sold units @ $25] |

35,00,000 |

40,00,000 |

|

|

(A) |

35,00,000 |

40,00,000 |

||

|

Variable cost: |

|

– |

|

|

|

|

Direct materials |

[production @ $5] |

8,50,000 |

7,00,000 |

|

|

Direct labour |

[production @ $6] |

10,20,000 |

8,40,000 |

|

|

Variable production cost |

[production @ $4] |

6,80,000 |

5,60,000 |

|

|

Cost of production (amount ÷ units = $15) |

25,50,000 |

24,00,000 |

|

|

Add: |

Beginning inventory |

[units @ $15] |

– |

4,50,000 |

|

Less: |

Ending inventory |

[units @ $15] |

(450,000) |

(150,000) |

|

|

COGS (B) |

21,00,000 |

24,00,000 |

|

|

|

Gross contribution (A – B) |

14,00,000 |

16,00,000 |

|

|

Less: |

Variable selling and admt cost |

[sales@5%] |

(175,000) |

(200,000) |

|

|

Net contribution |

12,25,000 |

14,00,000 |

|

|

Less: |

Fixed production cost |

|

(750,000) |

(750,000) |

|

|

Fixed selling and admt cost |

|

(325,000) |

(325,000) |

|

Net Income |

$1,50,000 |

$3,25,000 |

||

Income Statement under Absorption Costing

170,000 and 140,000 units

|

Particulars |

Year 2020 |

Year 2021 |

||

|

Sales revenue |

[sold units @ $25] |

35,00,000 |

40,00,000 |

|

|

(A) |

35,00,000 |

40,00,000 |

||

|

Manufacturing cost: |

|

– |

|

|

|

|

Direct materials |

[production @ $5] |

8,50,000 |

7,00,000 |

|

|

Direct labour |

[production @ $6] |

10,20,000 |

8,40,000 |

|

|

Variable production cost |

[production @ $4] |

6,80,000 |

5,60,000 |

|

|

Fixed production cost |

[production @ $5] |

8,50,000 |

7,00,000 |

|

|

Cost of production (amount ÷ units = $20) |

34,00,000 |

28,00,000 |

|

|

Add: |

Beginning inventory |

[units @ $20] |

– |

6,00,000 |

|

Less: |

Ending inventory |

[units @ $20] |

(600,000) |

(200,000) |

|

|

COGS before adjustment |

28,00,000 |

32,00,000 |

|

|

Add: |

Under absorption |

[compare with variable costing] |

– |

50,000 |

|

Less: |

Over absorption |

[compare with variable costing] |

1,00,000 |

– |

|

|

COGS after adjustment (B) |

27,00,000 |

32,50,000 |

|

|

|

Gross profit (A–B) |

8,00,000 |

7,50,000 |

|

|

Less: |

Variable selling and admt cost |

[sales@5%] |

(175,000) |

(200,000) |

|

Less: |

Fixed selling and admt cost |

|

(325,000) |

(325,000) |

|

Net Income |

$3,00,000 |

$2,25,000 |

||

Reconciliation Statement

|

Particulars |

Year 2020 |

Year 2021 |

|||

|

Net income as per variable costing |

150,000 |

325,000 |

|||

|

Add: Closing stock |

30,000 |

10,000 |

@ $5 |

150,000 |

50,000 |

|

Less: Opening stock |

Nil |

30,000 |

@ $5 |

Nil |

(150,000) |

|

Net income as per absorption costing |

$300,000 |

$225,000 |

|||

Closing stock of year 1 becomes opening stock of year 2, here $30,000

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 3C

ABC Manufacturing Company has following information related to a product:

|

Year |

Production |

Sales |

Sales price per unit |

|

2019 |

6,000 |

4,000 |

$300 |

|

2020 |

4,000 |

5,000 |

$300 |

|

2021 |

5,000 |

6,000 |

$300 |

Other information:

|

Normal production 5,000 units |

Variable cost per unit: |

Administrative and selling cost: |

|

|

Fixed production cost $500,000 |

Direct materials |

$60 |

Variable 5% of sales |

|

|

Direct labour |

$30 |

Fixed $100,000 |

|

|

Variable production cost |

$10 |

|

|

|

Total |

$100 |

|

Required: (1) Income statement under variable costing for 2019, 2020 and 2021

(2) Income statement under absorption costing for 2019, 2020 and 2021

(3) Reconciliation statement

[Answer: Variable costing: 2019= $140,000; 2020 = $325,000; 2021 = $510,000;

Absorption costing: 2019 = $340,000; 2020 = $225,000; 2021 = $410,000]

SOLUTION:

Given and working note:

Year 2019

|

Sold units |

= |

Opening stock + Production – Closing stock |

|

4,000 |

= |

Nil + 6,000 – Closing stock |

|

Closing stock |

= |

2,000 |

Closing stock of last year becomes opening stock of current year

Year 2020

|

Sold units |

= |

Opening stock + Production – Closing stock |

|

5,000 |

= |

2,000 + 4000 – Closing stock |

|

Closing stock |

= |

1,000 |

Year 2021

|

Sold units |

= |

Opening stock + Production – Closing stock |

|

6,000 |

= |

1,000 + 5000 – Closing stock |

|

Closing stock |

= |

Nil |

Fixed cost per unit [FCPU]

= Factory overhead old ÷ Normal output

= $500,000 ÷ 50,000 units

= $100

Income Statement under Variable Costing

6,000; 4,000 and 5,000 units

|

Particulars |

Year 2019 |

Year 2020 |

Year 2021 |

||

|

Sales revenue |

[sold units @ $200] |

12,00,000 |

15,00,000 |

18,00,000 |

|

|

(A) |

12,00,000 |

15,00,000 |

18,00,000 |

||

|

Variable cost: |

|

|

|

|

|

|

|

Direct materials |

[production @ $60] |

3,60,000 |

2,40,000 |

3,00,000 |

|

|

Direct labour |

[production @ $30] |

1,80,000 |

1,20,000 |

1,50,000 |

|

|

Variable production cost |

[production @ $10] |

60,000 |

40,000 |

50,000 |

|

|

Cost of production ($ ÷ units = $100) |

$6,00,000 |

$4,00,000 |

$5,00,000 |

|

|

Add: |

Beginning inventory |

[units @ $100] |

– |

2,00,000 |

1,00,000 |

|

Less: |

Ending inventory |

[units @ $100] |

(200,000) |

(100,000) |

Nil |

|

|

COGS (B) |

4,00,000 |

500,000 |

6,00,000 |

|

|

|

Gross contribution (A – B) |

800,000 |

10,00,000 |

12,00,000 |

|

|

Less: |

Variable selling and admt cost |

[sales@5%] |

(60,000) |

(75,000) |

(90,000) |

|

|

Net contribution |

7,40,000 |

9,25,000 |

11,10,000 |

|

|

Less: |

Fixed production cost |

|

(500,000) |

(500,000) |

(5,00,000) |

|

|

Fixed selling and admt cost |

|

(100,000) |

(100,000) |

(100,000) |

|

Net Income |

1,40,000 |

3,25,000 |

5,10,000 |

||

Income Statement under Absorption Costing

6,000; 4,000 and 5,000 units

|

Particulars |

Year 2019 |

Year 2020 |

Year 2021 |

||

|

Sales revenue |

[sold units @ $25] |

12,00,000 |

15,00,000 |

18,00,000 |

|

|

(A) |

12,00,000 |

15,00,000 |

18,00,000 |

||

|

Manufacturing cost: |

|

|

|

|

|

|

|

Direct materials |

[production @ $60] |

3,60,000 |

2,40,000 |

3,00,000 |

|

|

Direct labour |

[production @ $30] |

1,80,000 |

1,20,000 |

1,50,000 |

|

|

Variable production cost |

[production @ $10] |

60,000 |

40,000 |

50,000 |

|

|

Fixed production cost |

[production @ $100] |

6,00,000 |

4,00,000 |

5,00,000 |

|

|

Cost of production (amount ÷ units = $200) |

12,00,000 |

8,00,000 |

10,00,000 |

|

|

Add: |

Beginning inventory |

[units @ $200] |

– |

4,00,000 |

2,00,000 |

|

Less: |

Ending inventory |

[units @ $200] |

(400,000) |

(200,000) |

– |

|

|

COGS before adjustment |

8,00,000 |

10,00,000 |

12,00,000 |

|

|

Add: |

Under absorption |

[compare with variable costing] |

|

1,00,000 |

|

|

Less: |

Over absorption |

[compare with variable costing] |

1,00,000 |

|

|

|

|

COGS after adjustment (B) |

7,00,000 |

11,00,000 |

12,00,000 |

|

|

|

Gross profit (A–B) |

5,00,000 |

4,00,000 |

6,00,000 |

|

|

Less: |

Variable admt and selling cost |

[sales@5%] |

(60,000) |

(75,000) |

(90,000) |

|

Less: |

Fixed admt and selling cost |

|

(100,000) |

(100,000) |

(100,000) |

|

Net Income |

3,40,000 |

2,25,000 |

4,10,000 |

||

Reconciliation Statement

|

Particulars |

Year 2019 |

Year 2020 |

Year 2021 |

||||

|

Net income as per variable costing |

1,40,000 |

3,25,000 |

5,10,000 |

||||

|

Add: Closing stock |

2,000 |

1,000 |

Nil |

@ $100 |

2,00,000 |

1,00,000 |

Nil |

|

Less: Opening stock |

Nil |

2,000 |

1,000 |

@ $100 |

Nil |

(200,000) |

(100,000) |

|

Net income as per absorption costing |

3,40,000 |

2,25,000 |

4,10,000 |

||||

Closing stock of year 1 becomes opening stock of year 2, here $2,000 and 1,000

WHEN QUESTION IS GIVEN IN VARIABLE OR ABSORPTION COSTING

Sometime variable costing or absorption costing is given in the question.

In such a condition, you can be asked to calculate:

When question is given in variable costing you are asked to calculate absorption costing and reconciliation statement.

When question is given in absorption costing you are asked to calculate variable costing and reconciliation statement.

The Relationships between Production, Sales and Profit

|

Conditions |

Result |

Reason |

|

Sales = Production |

Profit of variable costing = Profit of absorption costing |

No change in inventory |

|

Sales > Production |

Profit of variable costing > Profit of absorption costing |

Decrease in inventory |

|

Sales < Production |

Profit of variable costing < Profit of absorption costing |

Increase in inventory |

Or

|

Profit of variable costing = Profit of absorption costing |

No change in inventory |

No opening , no closing stock* |

|

Profit of variable costing > Profit of absorption costing |

Decrease in inventory |

Opening stock > Closing stock |

|

Profit of variable costing < Profit of absorption costing |

Increase in inventory |

Opening stock < Closing stock |

*Sometime opening stock and closing stock may be equal.

Keep in Mind (KIM)

|

If production = sales, net income will be same for variable costing and absorption costing. |

|

If there are not opening stock and closing stock, net income of variable costing = absorption costing. |

|

If sales > production, net income of variable costing will be more than absorption costing. |

|

If sales < production, net income of variable costing will be less than absorption costing. |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 3D [production = sales]

Rupandehi Biscuits (P) Ltd keeps its accounting under variable costing system. Following data is available on 31st December:

Income Statement under Variable Costing

For 10,000 units

|

Particulars |

Amount |

|||

|

Sales revenue |

[10,000 units @ $20] |

200,000 |

||

|

(A) |

200,000 |

|||

|

Variable cost: |

|

|

||

|

|

Direct materials |

[10,000 units @ $2] |

20,000 |

|

|

|

Direct labour |

[10,000 units @ $3] |

30,000 |

|

|

|

Variable manufacturing cost |

[10,000 units @ $1.5] |

15,000 |

|

|

|

Cost of production |

65,000 |

||

|

Add: |

Beginning inventory |

[0 units @ $6.5] |

Nil |

|

|

Less: |

Ending inventory |

[0 units @ $6.5] |

Nil |

|

|

|

COGS (B) |

65,000 |

||

|

|

Gross contribution (A – B) |

135,000 |

||

|

Less: |

Variable administrative cost |

[10,000 @ $1] |

(10,000) |

|

|

Less: |

Variable S&D cost |

[10,000 @ $0.50] |

(5,000) |

|

|

|

Net contribution |

120,000 |

||

|

Less: |

Fixed manufacturing cost |

|

20,000 |

|

|

|

Fixed administrative cost |

|

10,000 |

|

|

|

Fixed selling and distribution cost |

|

+20,000 |

(50,000) |

|

Net Income |

$70,000 |

|||

Additional information:

Normal output is 20,000 units.

Production is 10,000 units and sales are 10,000 units.

Required: (1) Absorption Costing; (1) Reconciliation Statement

[Answer: Absorption costing = $70,000]

SOLUTION:

Fixed cost per unit [FCPU]

= Factory overhead ÷ Normal output

= $20,000 ÷ 20,000 unit

= $1

Income Statement under Absorption Costing

For 10,000 units

|

Particulars |

Amount |

|||

|

Sales revenue |

[10,000 units @ $20] |

200,000 |

||

|

(A) |

200,000 |

|||

|

Manufacturing cost: |

|

|

||

|

|

Direct materials |

[10,000 units @ $2] |

20,000 |

|

|

|

Direct labour |

[10,000 units @ $3] |

30,000 |

|

|

|

Variable production cost |

[10,000 units @ $1.5] |

15,000 |

|

|

|

Fixed manufacturing cost |

[10,000 units @ $1] |

10,000 |

|

|

|

Cost of production @ $7.5) |

75,000 |

||

|

Add: |

Beginning inventory |

[0 units @ $7.5] |

Nil |

|

|

Less: |

Ending inventory |

[0 units @ $7.5] |

Nil |

|

|

|

COGS before adjustment |

75,000 |

||

|

Add: |

Under absorption |

[$20,000 in V.C. – $10,000 A.C.] |

10,000 |

|

|

Less: |

Over absorption |

|

– |

|

|

|

COGS after adjustment (B) |

85,000 |

||

|

|

Gross profit (A–B) |

115,000 |

||

|

Less: |

Variable administrative cost |

|

10,000 |

|

|

|

Variable S&D cost |

|

5,000 |

|

|

Less: |

Fixed administrative cost |

|

20,000 |

|

|

|

Fixed S&D cost |

|

10,000 |

(45,000) |

|

Net Income |

70,000 |

|||

Reconciliation Statement

|

Particulars |

Amount |

|

Net income as per variable cost |

70,000 |

|

Add: Closing stock (0 units @ $1) |

|

|

Less: Opening stock (0 units @ $1) |

|

|

Net income as per absorption cost |

70,000 |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 3E [production < sales]

Duggar Snacks (P) Ltd manufactures brand Kurmure in three sizes: big, medium and small. It keeps its accounting in variable costing. The following information is related to medium size on 31st December:

Income Statement under Variable Costing

For 45,000 units

|

Particulars |

Amount |

|||

|

Sales revenue |

[50,000 units @ $20] |

10,00,000 |

||

|

(A) |

10,00,000 |

|||

|

Variable cost: |

|

|

||

|

|

Direct materials |

[45,000 units @ $3] |

135,000 |

|

|

|

Direct labour |

[45,000 units @ $2] |

90,000 |

|

|

|

Variable manufacturing cost |

[45,000 units @ $1] |

45,000 |

|

|

|

Cost of production |

270,000 |

||

|

Add: |

Beginning inventory |

[15,000 units @ $6] |

90,000 |

|

|

Less: |

Ending inventory |

[10,000 units @ $6] |

(60,000) |

|

|

|

COGS (B) |

300,000 |

||

|

|

Gross contribution (A – B) |

700,000 |

||

|

Less: |

Variable administrative cost |

[45,000 @ $0] |

Nil |

|

|

Less: |

Variable S&D cost |

[50,000 @ $1] |

(50,000) |

|

|

|

Net contribution |

650,000 |

||

|

|

Fixed manufacturing cost |

|

150,000 |

|

|

|

Fixed administrative cost |

|

50,000 |

|

|

|

Fixed selling and distribution |

|

200,000 |

(400,000) |

|

Net Income |

250,000 |

|||

Additional information:

· Normal output is 50,000 units.

· Production is 45,000 units and sales are 50,000 units.

Required: (a) Absorption costing; (b) Reconciliation statement

[Answer: Absorption costing = $235,000]

SOLUTION:

Fixed cost per unit [FCPU]

= Fixed overhead ÷ Normal output

= $150,000 ÷ 50,000 units

= $3

Income Statement under Absorption Costing

For 45,000 units

|

Particulars |

Amount |

|||

|

Sales revenue |

[50,000 units @ $20] |

10,00,000 |

||

|

(A) |

10,00,000 |

|||

|

Manufacturing cost: |

|

– |

||

|

|

Direct materials |

[45,000 units @ $3] |

1,35,000 |

|

|

|

Direct labour |

[45,000 units @ $3] |

90,000 |

|

|

|

Variable production cost |

[45,000 units @ $1] |

45,000 |

|

|

|

Fixed manufacturing cost |

[45,000 units @ $3] |

1,35,000 |

|

|

|

Cost of production @ $9) |

4,05,000 |

||

|

Add: |

Beginning inventory |

[15,000 units @ $9] |

1,35,000 |

|

|

Less: |

Ending inventory |

[10,000 units @ $9] |

(90,000) |

|

|

|

COGS before adjustment |

4,50,000 |

||

|

Add: |

Under absorption |

[150,000 in VC – 135,000 AC] |

15,000 |

|

|

Less: |

Over absorption |

|

– |

|

|

|

COGS after adjustment (B) |

4,65,000 |

||

|

|

Gross profit (A–B) |

5,35,000 |

||

|

Less: |

Variable administrative cost |

|

Nil |

|

|

|

Variable S&D cost |

|

50,000 |

|

|

Less: |

Fixed administrative cost |

|

50,000 |

|

|

|

Fixed S&D cost |

|

200,000 |

(300,000) |

|

Net Income |

235,000 |

|||

Reconciliation Statement

|

Particulars |

Amount |

|

Net income as per Variable Cost |

250,000 |

|

Add: Closing stock (10,000 units @ $3) |

30,000 |

|

Less: Opening stock (15,000 units @ $3) |

(45,000) |

|

Net income as per Absorption Cost |

235,000 |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 3F [production > sales]

Cello Writing Instrument (P) Ltd manufactures different kinds of ball pens. The following information is obtained for particular ball pen on 31st December:

Income Statement under Absorption Costing

For 50,000 units

|

Particulars |

Amount |

|||

|

Sales revenue |

[45,000 units @ $20] |

900,000 |

||

|

(A) |

900,000 |

|||

|

Manufacturing cost: |

|

|

||

|

|

Direct materials |

[50,000 units @ $3] |

150,000 |

|

|

|

Direct labour |

[50,000 units @ $2] |

100,000 |

|

|

|

Variable production cost |

[50,000 units @ $1] |

50,000 |

|

|

|

|

|

|

|

|

|

Fixed manufacturing cost |

[50,000 units @ $3] |

150,000 |

|

|

|

Cost of production @ $9 |

450,000 |

||

|

Add: |

Beginning inventory |

[15,000 units @ $9] |

135,000 |

|

|

Less: |

Ending inventory |

[10,000 units @ $9] |

(90,000) |

|

|

|

COGS before adjustment |

495,000 |

||

|

Add: |

Under absorption |

|

15,000 |

|

|

|

COGS after adjustment (B) |

510,000 |

||

|

|

Gross profit (A–B) |

390,000 |

||

|

Less: |

Variable administrative cost |

|

30,000 |

|

|

|

Variable S & D cost |

[45,000 units @ $1] |

45,000 |

|

|

Less: |

Fixed administrative cost |

|

50,000 |

|

|

|

Fixed selling and distribution cost |

|

100,000 |

(225,000) |

|

Net Income |

$165,000 |

|||

Required: (1) Variable costing; (2) Reconciliation statement

[Answer: (1) $180,000; (2) $Different of stock value (45,000 – 30,000) = $15,000;

Hints: Fixed manufacturing cost = $165,000]

SOLUTION:

Income Statement under Variable Costing

For 50,000 units

|

Particulars |

Amount |

|||

|

Sales revenue |

[45,000 units @ $20] |

900,000 |

||

|

(A) |

900,000 |

|||

|

Variable cost: |

|

|

||

|

|

Direct materials |

[50,000 units @ $3] |

150,000 |

|

|

|

Direct labour |

[50,000 units @ $2] |

100,000 |

|

|

|

Variable manufacturing cost |

[50,000 units @ $1] |

50,000 |

|

|

|

Cost of production @ $6) |

300,000 |

||

|

Add: |

Beginning inventory |

[15,000 units @ $6] |

90,000 |

|

|

Less: |

Ending inventory |

[10,000 units @ $6] |

(60,000) |

|

|

|

COGS (B) |

330,000 |

||

|

|

Gross contribution (A – B) |

570,000 |

||

|

Less: |

Variable administrative cost |

[given] |

(30,000) |

|

|

Less: |

Variable S&D cost |

[45,000 @ $1] |

(45,000) |

|

|

|

Net contribution |

495,000 |

||

|

Less: |

Fixed manufacturing cost |

[$150,000 AC + $15,000 under absorbed] |

165,000 |

|

|

|

Fixed administrative cost |

[given] |

50,000 |

|

|

|

Fixed S&D cost |

[given] |

100,000 |

(315,000) |

|

Net Income |

180,000 |

|||

Reconciliation Statement

|

Particulars |

Amount |

|

Net income as per absorption costing |

165,000 |

|

Add: Opening stock (15,000 units @ $3) |

45,000 |

|

Less: Closing stock (10,000 units @ $3) |

(30,000) |

|

Net income as per variable costing |

180,000 |

Fixed manufacturing cost per unit given in the question $3

Click on the photo for FREE eBooks

#####

Problems and Answers of Absorption and Variable Costing |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 3A

Max Company uses direct costing for internal control purchase and absorption costing for external reporting purpose. The following differences are located while comparing the two statements.

|

Items |

Variable Costing |

Absorption Costing |

|

|

Variable manufacturing cost |

$60,000 |

$60,000 |

|

|

Fixed manufacturing cost charged |

$25,000 |

$30,000 |

|

|

Fixed selling and administrative cost |

$40,000 |

$40,000 |

|

|

Variable selling cost per unit |

$2 |

$2 |

|

|

Selling price per unit |

$30 |

$30 |

|

Management also projected the following data for the inventory:

|

Beginning inventory units 1,000 |

Sales units 5,000 |

|

Production units 6,000 |

Closing stock units 2,000 |

Cost of beginning inventory is the same as the cost of production in the period.

Required: Income statement by using absorption costing and variable costing approach

[Answers: Net profit = $30,000; $25,000]

*Over absorption $5,000]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 3B

XYZ Ltd uses direct costing for internal control purposes and absorption costing for external reporting purposes. The company uses the following unit costs for the one product it manufactures:

Projected cost per unit:

Direct materials $60

Direct labour $38

Variable manufacturing $12

Fixed manufacturing cost $10 (Based on 10,000 units per month)

Variable selling and administrative cost $8

Fixed selling and administrative cost $5.60 (Based on 10,000 units per month)

The projected selling price is $160 per unit.

The fixed costs remain fixed within the relevant range of 4,000 to 16,000 units of production.

Management has also projected the following data for the month:

Opening stock 2,000 units

Production 9,000 units

Sales 7,500 units

Required: projected income statement under direct costing and absorption costing.

[Answer: Variable costing: $1,59,000, Absorption costing: $1,74,000;

* Under absorption cost =100,000 – 90,000 = 10,000]

EP Online Study

Thank you for investing your time.

Please comment on the article.

You can help us by sharing this post on your social media platform.

Jay Google, Jay YouTube, Jay Social Media

जय गूगल. जय युट्युब, जय सोशल मीडिया

The post Absorption costing | Variable costing | Reconciliation Statement | Problems and solutions appeared first on EP Online Study.

]]>The post Variable Costing | Absorption vs Variable | Problems and Solutions appeared first on EP Online Study.

]]>

Variable Costing | Internal Costing | Direct Costing

Variable costing is also known as internal costing, direct costing and marginal costing.

Variable cost helps to administrator to solve the problem about production planning.

Under this method, production cost is calculated on variable basis.

Variable costing includes direct materials, direct labour and variable manufacturing cost in product cost.

It includes fixed manufacturing cost, administrative, selling and distribution cost in period cost.

Direct materials, direct labour, variable manufacturing cost:

= Production units x Cost per unit

Period costing under variable costing = Fixed manufacturing cost + Administrative cost + S&D cost

Total variable, selling and distribution cost = Sales units x Cost per unit

Sold units = Opening stock + Production – Closing stock

Variable costing | Cost allocation

Keep in Mind (KIM)

|