The post Standard Costing | Material Variance | Labour Variance | BQ | DQ | AQ appeared first on EP Online Study.

]]>

Standard Costing

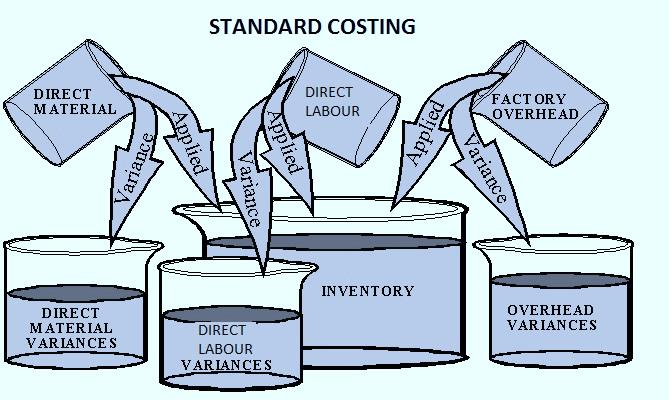

Standard costing is pre-determined cost.

It is determined in advance of production like cost of materials, wages or labour, overheads etc.

It is a management accounting tools for management control.

It is applied to compare the actual cost with variance.

It is used for following process:

Establishment of standard cost

To find out actual cost

To compare and measurement of variance

Analysis of variances

Reporting to related center for taking action

Materials

In a manufacturing company, materials and labour are the most important factors for production.

Raw materials are converted into semi-finished goods and finished goods with the help of labour.

While manufacturing the goods, all the input goods are NOT output or yield.

There are normal and abnormal losses.

When the company cannot stop or control the loss of goods on a natural basis; it is called normal loss.

Normal losses are weight loss, shrinkage, evaporation, rust etc.

When the company can stop or control loss but could not control, it is known as abnormal loss.

Abnormal loss is due to carelessness, fatigue, rough handling, abnormal or bad working condition, lack of proper knowledge, low-quality raw materials, machine break down, accidents etc.

We will study the following materials variances in this topic:

Materials cost variance

Materials price variance

Materials usage variance

Materials mix variance

Materials yield variance

Click on the photo for FREE eBooks

Labour

Every manufacturing company and business organization needs human being resources.

These human beings may be the resource of administrators and labour.

Without labour, a manufacturing company cannot complete its production.

It is saying, “Talented, calibre and skilled manpower is the other assets of the business organization.”

There are three types of labour.

They are unskilled labour, semi-skilled labour and skilled labour.

Unskilled labour gets fewer wages but skilled labour gets the highest wages.

The payment made to the labour in exchange for its service is called labour cost.

It is a major part of the total cost of production.

Labour cost is also commonly called wages.

Labour cost or wages is one of the major elements of cost.

Labour cost represents the expense incurred on both direct and indirect labour.

Unproductive time is known as idle time.

It may be due to normal or abnormal reasons.

In idle time, workers have been paid without any production activity.

To identify the reasons for the idle time in the factory, an idle time card is maintained.

We will study the following labour variances in this topic:

Labour rate variance

Labour efficiency variance

Labour idle time variance

Labour mix variance

Labour yield variance

Labour cost variance

Brief Questions

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 1

Following data is available for materials X:

|

Standard rate of materials per kg |

$40 |

Actual materials consumed |

2,200 kg |

|

Standard quality of materials |

2,000 kg |

Actual rate of materials per kg |

$38 |

|

Standard rate of standard mix |

$80,000 |

Actual rate of actual mix |

$83,600 |

Required: (three variances of materials)

(a) Materials price variance; (b) Materials usage variance; (c) Materials cost variance

[Answer: MPV = $4,400 F; MUV = $8,000 U; MVC = $3,600 U]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 2

The following data related to materials are given:

|

Standard materials mix |

Actual materials mix |

||||

|

Materials |

kg |

Rate per kg |

Materials |

Units |

Rate per kg |

|

X |

500 |

50 |

X |

600 |

45 |

Required: (a) Materials price variance; (b) Materials usage variance; (c) Materials cost variance

[Answer: MPV = $3,000 F; MUV = $5,000 U; MCV = $2,000 U]

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

BQ: 3

The following extracted data are given:

|

|

Standard |

Actual |

||||

|

Labour |

No./mix |

Rate ($) |

Cost |

No./mix |

Rate($) |

Cost |

|

Trainee |

1,000 |

25 |

25,000 |

1,100 |

22.50 |

24,750 |

Required: (a) Labour rate variance; (b) Labour efficiency variance; (c) Labour cost variance

[Answer: LRV = $2,750 F; LEV = $2,500 U; LCV = $250 F]

######

|

Click on the link for YouTube videos |

|

|

Accounting Equation |

|

|

Journal Entries in Nepali |

|

|

Journal Entries |

|

|

Journal Entry and Ledger |

|

|

Ledger |

|

|

Subsidiary Book |

|

|

Cashbook |

|

|

Trial Balance and Adjusted Trial Balance |

|

|

Bank Reconciliation Statement (BRS) |

|

|

Depreciation |

|

|

|

|

|

Click on the link for YouTube videos chapter wise |

|

|

Financial Accounting and Analysis (All videos) |

|

|

Accounting Process |

|

|

Accounting for Long Lived Assets |

|

|

Analysis of Financial Statement |

|

######

Descriptive Questions

Materials Variances

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 1

The following data related to materials are given:

|

Standard materials mix |

Actual materials mix |

||||||

|

Materials |

Units |

Rate |

Amount |

Materials |

Units |

Rate |

Amount |

|

A |

600 |

15 |

9,000 |

A |

500 |

24 |

12,000 |

|

B |

200 |

35 |

7,000 |

B |

100 |

60 |

6,000 |

There is not any loss during production.

Required: (a) Materials price variance; (b) Materials mix variance; (c) Materials usage variance; (d) Materials cost variance

[Answer: MPV = $7,000 U; MMV = $1,000 F; MUV = $5,000 F;

MCV = $2,000 U* SP1 = 18.33; SP2 = 20

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 2

The following data related to materials are given:

|

Standard materials mix |

Actual materials mix |

||||

|

Materials |

Kg |

Rate |

Materials |

Kg |

Rate |

|

M |

200 |

20 |

M |

100 |

35 |

|

N |

400 |

25 |

N |

200 |

20 |

|

O |

400 |

30 |

O |

500 |

25 |

Standard and actual outputs were 1,000 units. Standard loss is 10% and actual output is 750 units.

Required: (a) Materials price variance; (b) Materials mix variance; (c) Materials yield variance; (d) Materials usage variance;

(e) Materials cost variance

[Answer: MPV = $2,000 F; MMV = $1,200 U;

MYV = $867 F; MUV = $333 U;

MCV = $1,667 F *SP1 = 27.50; SP2 = 26; SP3 = 28.889

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 3

The standards cost for a product of the company shows the following materials standard:

|

Standard |

Actual |

||||

|

Materials |

Quantity |

price per kg |

Materials |

Quantity |

price per kg |

|

A |

4 kg |

$5 |

A |

150 kg |

$4 |

|

B |

1 kg |

$10 |

B |

40 kg |

$10 |

|

C |

5 kg |

$20 |

C |

210 kg |

$25 |

The standard loss is 10% Actual output of the finished product is 380 kg.

Required: (1) (a) Material mixed variance; (b) Material yield variance; (c) Material price variance

(2) Write down any four advantages of standard costing

[Answer: MPV = $900 U; MMV = $150 U; MYV = ($287) F]

*SP1 = 13.375; SP2 = 13; SP3 = 14.44

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 4

The following details material standard and consumption have been provided

|

Materials |

Standard |

Actual |

||||

|

Quantity |

Rate |

Cost |

Quantity |

Rate |

Cost |

|

|

A |

2 |

4 |

8 |

190 |

4.00 |

760 |

|

B |

3 |

3 |

9 |

290 |

3.00 |

899 |

|

C |

5 |

2 |

10 |

510 |

1.80 |

918 |

|

|

10 |

|

$27 |

990 |

|

$2,577 |

Standard output 8 units and actual output 800 units

Required: (a) Material yield variance; (b) Materials mix variance; (c) Materials use variance; (d) Materials price variances

[Answer: MPV = ($73) F; MMV = ($23) F; MYV = ($27) F; MUV = ($50) F]

SP1 = 2.677; SP2 = 2.7; SP3 = 3.375

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 5

The details regarding materials are:

|

Materials |

Standard |

Material consumed |

||||

|

|

Quantity in units |

Price |

Cost |

Quantity in units |

Price |

Cost |

|

A |

30 |

$3 |

$90 |

280 |

$2.75 |

$770 |

|

B |

30 |

$2 |

$60 |

265 |

$2.00 |

$530 |

|

C |

40 |

$1 |

$40 |

375 |

$1.20 |

$450 |

|

|

100 |

|

$190 |

920 |

|

$1,750 |

Standard loss 20% and Actual output 720 units

Required: (a) Material yield variance; (b) Materials mix variance; (c) Materials usage variance; (d) Materials price variances

[Answer: MPV = $5 U; MMV = ($3) F; MYV = $38 U; MUV = $35 U]

SP1 = 1.897; SP2 = 1.9; SP3 = 2.375

Labour Variances

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 6

The following extracted information is available:

|

Labour |

Standard |

Actual |

||

|

No. of workers |

Wage rate per hour |

No. of workers |

Wage rate per hour |

|

|

Semi -skilled |

200 |

$37.50 |

220 |

$36.00 |

|

Unskilled |

100 |

$22.50 |

80 |

$24.00 |

Standard time fixed for work 50 hours. Work actually completed in also 50 hours.

Required: (Direct) (a) Labour rate variance; (b) Labour mix variance; (c) Labour efficiency variance; (d) Labour cost variances

[Answer: LRV = $10,500 F; LMV = $15,000 U; LEV = $15,000 U;

LCV = $4,500 U] *SR1 = 10,050; SR2 = 9,750;

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 7

ABC Company gives you following standard and actual data:

|

Standard |

Actual |

||||||

|

Workers |

No. |

Rate per hour |

Hours worked |

Workers |

No. |

Rate per hour |

Hours Worked |

|

Grade A |

50 |

$50 |

100 |

Grade A |

30 |

$75 |

120 |

|

Grade B |

100 |

$25 |

100 |

Grade B |

120 |

$20 |

120 |

Required: (a) Labour mix variance; (b) Labour efficiency variance; (c) Labour rate variance; (d) Labour yield variance

[Answer: LRV = $18,000 U; LMV = ($60,000) F; LYV = $100,000 U;

LEV = $40,000 U] *SR1 = 4500; SR2 = 5000;

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 8

The following extracted data related to labour of ABC Company has given below:

|

Standard |

Actual |

||||

|

Labour |

Hour per unit |

Rate per hour |

Labour |

Hours per unit |

Rate per hour |

|

Skilled |

5 |

37.50 |

Skilled |

4.5 |

50.00 |

|

Semi-skilled |

4 |

18.75 |

Semi-skilled |

4.2 |

18.75 |

|

Unskilled |

8 |

12.50 |

Unskilled |

10 |

11.25 |

Standard and actual productions were 1,000 units. Standard and actual gang time 48 hours in a week.

Required: (Direct): (a) Labour rate variance; (b) Labour mix variance; (c) Labour yield variance; (d) Labour efficiency variance;

(d) Labour cost variances

[Answer: LRV = $2,100 U; LMV = $480 U; LYV = Nil; LEV = $480 U;

LCV = $2,580 U; *SR1 = 372.5; SR2 = 362.5; SR3 = 17.40

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

DQ: 9

The details regarding labor cost have been provided as:

|

Type |

Standard |

Actual |

||||

|

No. |

Rate/Hour |

Cost |

No. |

Rate/Hour |

Cost |

|

|

Skilled |

1 |

$50 |

50 |

1 |

$45 |

45 |

|

Semi- skilled |

3 |

$30 |

90 |

4 |

$30 |

120 |

|

Unskilled |

6 |

$20 |

120 |

5 |

$22 |

110 |

|

|

10 |

|

260 |

10 |

|

275 |

40 hours a week needed to work and paid. Actual output produced 360 units. Standard output per gang hour is 8 units.

Required: (direct): (a) Labour rate variance; (b) Labour mix variance; (c) Labour efficiency sub (yield) variance;

(d) Labour efficiency variance; (e) Labour cost variance

[Answer: LRV = $200 U; LMV = $400 U; LYV = ($1,300) F; LEV = ($900) F;

LCV = ($700) F] *SR1 = 270; SR2 = 260; SR3 = 32.5

Click on the photo for FREE eBooks

ACCOUNTING, ECONOMICS, BUSINESS STUDIES, FINANCE, ENGLISH eBooks, EP Online Study

Analytical Questions

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 1

ABC Manufacturing Company provides you following information related to materials.

|

Standard materials cost with 1 ton output were: |

Actual materials cost with 1,000 kg output were: |

||

|

Materials A |

300 kg at $100 |

Materials A |

0.35 tons at $90,000 per ton |

|

Materials B |

400 kg at $50 |

Materials B |

0.42 tons at $60,000 per ton |

|

Materials C |

500 kg at $60 |

Materials C |

0.53 tons at $70,000 per ton |

Required: (a) Materials price variance; (b) Materials mix variance; (c) Materials yield variance; (d) Materials usage variance;

(e) Materials cost variance

MPV = $6,000 U; MPV = $1,113 U; MYV = $6,667 U;

MUV = $7,800 U; MCV = $13,800 U]

* 1 ton = 1,000 kg] *SP1 = 67.538; SP2 = 66.667; SP3 = 80

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 2

XYZ Company (P) Ltd has information:

|

Standard |

Actual |

||||

|

Labour |

No./mix |

Rate ($) |

Labour |

No./mix |

Rate ($) |

|

Skilled |

10 |

50 |

Skilled |

13 |

48 |

|

Semi-skilled |

5 |

32 |

Semi-skilled |

4 |

34 |

|

Unskilled |

5 |

28 |

Unskilled |

3 |

26 |

|

Total |

20 |

|

Total |

20 |

|

|

Normal working hours (STG) 40 hours |

Actual output realized 960 hours |

||||

|

Standard output 1,000 |

Abnormal idle time 2 hours |

||||

Required: (a) Labour rate variance; (b) Labour ideal time variance; (c) Labour mix variance; (d) Labour yield variance;

(e) Labour efficiency variance; (f) Labour cost variance

[Answer: LRV = ($960) F; LITV = $1,724 U; LMV = $2,356 U;

LYV = ($320) F; LEV = $3,760 U; LCV = $2,800 U]

*SR1 = 862; SR2 = 800; SR3 = 32

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 3

APD Power (P) Ltd has following labour data:

|

Standard |

Actual |

||||

|

Labour |

No. |

Rate per hour ($) |

Labour |

No. |

Rate per hour ($) |

|

Grade A |

30 |

48 |

Grade A |

40 |

42.00 |

|

Grade B |

15 |

36 |

Grade B |

10 |

40.80 |

|

Grade C |

10 |

24 |

Grade C |

5 |

18.00 |

Normal working hours in week is 40 hours. Standard yield was 1,600 units. It is expected to produce by gang 2,000 hours during the period but actual yield was 1,980 hours due to four abnormal idle times.

Required: (a) Labour rate variance; (b) Labour ideal time variance; (c) Labour mix variance; (d) Labour yield variance;

(e) Labour efficiency variance; (f) Labour cost variance

[Answer: LRV = ($8,880) F; LITV = $2,400 U; LMV = $7,020 U;

LEV = ($23,310) F; LEV = ($13,890) F; LCV = ($22,770) F]

[Answer: LRV = ($4,040) F; LITV = $1,200 U; LMV = $3,510 U;

LYV = ($11,655) F; LEV = ($6,945) F; LCV = ($11,385) F]

*SR1 = 2,400; SR2 = 2,220; SR3 = 55.50

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

AQ: 4

ABC Manufacturing Company has following data related to materials and labour:

|

Standard |

Actual |

||||

|

Kg |

Materials |

Rate |

Kg |

Materials |

Rate |

|

450 |

A |

20 |

450 |

A |

19 |

|

360 |

B |

10 |

360 |

B |

11 |

|

|

|

|

|

|

|

|

Hours |

Labour |

Rate |

Hours |

Labour |

Rate |

|

2,400 |

Skilled |

40 |

2,400 |

Skilled |

45 |

|

1,200 |

Unskilled |

20 |

1,200 |

Unskilled |

25 |

For materials as well as labour, standard loss is 90 kg and actual yield is 760 kg.

Required: (Direct)

|

Materials price variance |

Labour rate variance |

|

Materials mix variance |

Labour mix variance |

|

Materials yield variance |

Labour yield variance |

|

Materials efficiency/usage variance |

Labour efficiency/use |

|

Materials cost variance |

Labour cost variance |

[Answer for materials: MPV = ($90) U; MMV = Nil; MYV = ($700) F;

MUV = ($700) F; MCV = ($790) F]

SP1 = 15.556; SP2 = 15.556; SP3 = 17.5

[Answer for labour: LRV = $18,000 U; LMV = Nil; LYV = ($6,669) F;

LEV = ($6,669) F; LCV = $11,331 U]

SR1 = 120,000; SR2 = 120,000; SR3 = 166.67

EP Online Study

Thank you for investing your time.

Please comment on the article and share this post on your social media platform.

Jay Google, Jay YouTube, Jay Social Media

जय गूगल. जय युट्युब, जय सोशल मीडिया

The post Standard Costing | Material Variance | Labour Variance | BQ | DQ | AQ appeared first on EP Online Study.

]]>The post Labour Variance | Rate | Efficiency | Idle Time | Mix | Yield | Cost | Problem & Solution appeared first on EP Online Study.

]]>

Materials

In a manufacturing company, materials and labour are the most important factors for production.

Raw materials are converted into semi-finished goods and finished goods with the help of labour.

While manufacturing the goods, all the input goods are NOT output or yield.

There are normal and abnormal losses.

When the company cannot stop or control the loss of goods on a natural basis; it is called normal loss.

Normal losses are weight loss, shrinkage, evaporation, rust etc.

When the company can stop or control loss but could not control, it is known as abnormal loss.

Abnormal loss is due to carelessness, fatigue, rough handling, abnormal or bad working condition, lack of proper knowledge, low-quality raw materials, machine break down, accidents etc.

We will study the following materials variances in this topic:

Materials cost variance

Materials price variance

Materials usage variance

Materials mix variance

Materials yield variance

Click on the photo for FREE eBooks

Labour

Every manufacturing company and business organization needs human being resources.

These human beings may be the resource of administrators and labour.

Without labour, a manufacturing company cannot complete its production.

It is saying, “Talented, calibre and skilled manpower is the other assets of the business organization.”

There are three types of labour.

They are unskilled labour, semi-skilled labour and skilled labour.

Unskilled labour gets fewer wages but skilled labour gets the highest wages.

The payment made to the labour in exchange for its service is called labour cost.

It is a major part of the total cost of production.

Labour cost is also commonly called wages.

Labour cost or wages is one of the major elements of cost.

Labour cost represents the expense incurred on both direct and indirect labour.

Unproductive time is known as idle time.

It may be due to normal or abnormal reasons.

In idle time, workers have been paid without any production activity.

To identify the reasons for the idle time in the factory, an idle time card is maintained.

We will study the following labour variances in this topic:

Labour rate variance

Labour efficiency variance

Labour idle time variance

Labour mix variance

Labour yield variance

Labour cost variance

Direct Labour Variance | Labour Variance

Every production company needs labour for production.

By using the labour, the company produces goods.

While producing the goods, there may be variances.

A labour variance arises when the actual cost varies from expected budgeted or standard amount.

This varies either better or worse.

The difference between standard cost of labour and actual cost of labour is labour/wage variance.

Direct labour cost variance is the difference between the standard cost for actual production and the actual cost in production.

There are two kinds of labour variances.

They are labour rate variance and labour efficiency variance.

Labour rate variance is the difference between the standard cost and the actual cost paid for the actual number of hours.

Labour efficiency variance is the difference between the standard labour hours.

The principle of labour cost variance is similar to materials cost variance.

Purchase of materials, usage of materials and usage of labour are connected with each other.

Before finding out labour variances, the following point should be found out (requirement for labour variance):

|

AR |

= Actual wage rate per period (hour, day, week, month) |

|

AT or AQ |

= Actual time taken or actual quantity used for production |

|

SR |

= Standard wage rate per period (hour, day, week, month) |

|

ST or SQ |

= Standard time or standard quantity used for production |

|

SY or SO |

= Standard yield or output |

|

AY or AO |

= Actual yield or output |

|

RSY |

= Revised standard yield |

|

IT |

= Idle time |

|

AGT |

= Actual gang time |

|

SGT |

= Standard gang time |

|

SR1 |

= standard rate per unit of actual mix |

|

SR2 |

= standard rate per unit of standard mix |

|

SR3 |

= standard rate |

|

|

|

|

Types of labour variance |

|

|

Labour Rate Variance (LRV) |

|

|

Labour Efficiency Variance (LEV) |

|

|

Labour Idle Time Variance (LITV) |

|

|

Labour Mix Variance (LMV) |

|

|

Labour Yield Variance (LYV) |

|

|

Labour Cost Variance (LCV) |

|

(1) Labour cost variance, LCV

The difference between standard direct labour cost for actual activity and direct labour cost paid is known as direct labour cost variance.

|

LCV |

= (Standard time × Standard rate) – (Actual time × Actual rate) |

|

Or |

= (ST × SR) – (AT × AR) |

(2) Labour rate variance, LRV

The difference between standard wage rates fixed and actual wage paid as known labour rate variance.

|

LRV |

= Actual time × (Standard rate – Actual rate) |

|

Or |

= AT × (SR – AR) |

(3) Labour efficiency variance, LEV

The difference between labour hours specified for the activity achieved and actual labour hour expended as known labour efficiency variance.

|

LEV |

= Standard rate × (Standard time – Actual time) |

|

Or |

= SR × (ST – AT) |

Three (3) variances without mix and yield variances

|

Computation: |

Variances: |

by table |

by formula |

|

L1 = AT × AR |

Labour Rate Variance (LVR) |

= L1 – L2 |

= AT (SR– AR) |

|

L2 = AT × SR |

Labour Efficiency Variance (LEV) |

= L2 – L3 |

= SR (ST– AT) |

|

L3 = ST × SR |

Labour Cost Variance (LCV) |

= L1 – L3 |

= (ST × SR) – (AT × AR) |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 2A

The following data related to labour are given below by HP Company (P) Ltd:

|

Standard labour mix |

Actual labour mix |

||||

|

Labour |

Hours/No. |

Rate per hour |

Labour |

Hours/No. |

Rate per hour |

|

Skilled |

200 |

$50 |

Skilled |

150 |

$60 |

Required: (1) Labour rate variance; (2) Labour efficiency variance; (3) Labour cost variance

[Answer: LRV = $(1,500) U; LEV = $2,500 F; LCV = $1,000 F]

SOLUTION:

By table method:

Given and working note:

|

Labour |

Standard |

Actual |

Standard × Actual |

||||

|

|

No. (ST) |

Rate (SR) |

Amount |

No. (AT) |

Rate (AR) |

Amount |

SR × AT |

|

Skilled |

200 |

50 |

10,000 |

150 |

60 |

9,000 |

50 × 150 = 7,500 |

|

Total |

200 |

|

SR2 =10,000 |

150 |

|

9,000 |

SR1 = 7,500 |

Again,

L1 = AT × AR = 150 × 60 = $9,000

L2 = AT × SR = 150 × 50 = $7,500

L3 = ST × SR = 200 × 50 = $10,000

Now,

|

Labour Rate Variance (LRV) |

= L1 – L2 |

= 9,000 – 7,500 |

= $1,500 U |

|

Labour Efficiency Variance (LEV) |

= L2 – L3 |

= 7,500 – 10,000 |

= $(2,500) F |

|

Labour Cost Variance(LCV) |

= L1 – L3 |

= 9,000 – 10,000 |

= $(1,000) F |

By formula method:

Labour rate variance (LRV)

= Actual time × (Standard rate – Actual rate)

= AT × (SR – AR)

= 150 (50 – 60)

= 150 × – 10

= ($1,500) U

Labour Efficiency Variance (LEV)

= Standard rate × (Standard time – Actual time)

= SR × (ST – AT)

= 50 × (200 – 150)

= 50 × 50

= $2,500 F

Labour cost variance (LCV)

= (Standard time × Standard rate) – (Actual time × Actual rate)

= (ST × SR) – (AT × AR)

= (200 × 50) – (150 × 60)

= 10,000 – 1,000

= $1,000 F

Keep in Mind (KIM)

|

Formula method |

Table method |

|

Positive result or answer means favorable (F) Negative result or answer means un-favourable (U) or adverse (A) |

Positive result or answer means unfavourable (U) or adverse (A) Negative result or answer means favourable (F) |

(4) Labour idle time variance, LITV

Labour idle time arises is due to abnormal wastage of time like strike, lock out, power failure, machinery break down etc.

Idle time variance is always adverse (unfavorable).

It is needed investigation for its causes.

It shows in-efficiency of workers although they are not responsible for this.

|

LITV |

= Idle time × Standard rate |

|

Or |

= IT × SR |

Four (4) variances without mix and yield variances

|

Computation: |

Variances: |

by table |

by formula |

|

L1 = AT × AR |

Labour Rate Variance (LRV) |

= L1 – L2 |

= AT × (SR– AR) |

|

L2 = AT × SR |

Labour Ideal Time Variance (LITV) |

= L2 – L3 |

= SR × IT |

|

L3 = (AT – IT) SR |

Labour Efficiency Variance (LEV) |

= L3 – L4 |

= SR × (ST– AT) |

|

L4 = ST × SR |

Labour Cost Variance (LCV) |

= L1 – L4 |

= (ST × SR) – (AT × AR) |

Keep in Mind (KIM)

|

Labour idle time variance is always unfavourable either positive or negative answer |

######

|

Click on the link for YouTube videos |

|

|

Accounting Equation |

|

|

Journal Entries in Nepali |

|

|

Journal Entries |

|

|

Journal Entry and Ledger |

|

|

Ledger |

|

|

Subsidiary Book |

|

|

Cashbook |

|

|

Trial Balance and Adjusted Trial Balance |

|

|

Bank Reconciliation Statement (BRS) |

|

|

Depreciation |

|

|

|

|

|

Click on the link for YouTube videos chapter wise |

|

|

Financial Accounting and Analysis (All videos) |

|

|

Accounting Process |

|

|

Accounting for Long Lived Assets |

|

|

Analysis of Financial Statement |

|

######

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 2B

The following data related to labour are given below by ABC Manufacturing Company:

|

Standard labour mix |

Actual labour mix |

||||

|

Labour |

Hours/No. |

Rate per hour |

Labour |

Hours/No. |

Rate per hour |

|

Unskilled |

1,920 |

$24 |

Skilled |

2,000 |

$27 |

Additional information:

Due to power failed of machinery, 20% of actual hours were idle time.

Standard time was 40 hours in a week.

Required: (a) Labour Rate Variance (LRV); (b) Labour Ideal Time Variance (LITV); (c) Labour Efficiency Variance (LEV);

(d) Labour Cost Variance (LCV)

[Answer: LVR = $6,000 U; LITV = $9,600 U;

LEV = $7,680 F; LCV = $7,920 U]

SOLUTION:

By table method:

Given and working note:

|

Labour |

Standard |

Actual |

Standard × Actual |

||||

|

|

SN |

SR |

Amount |

AN |

AR |

Amount |

SR × AT |

|

Unskilled |

1,920 |

24 |

46,080 |

2,000 |

27 |

54,000 |

24 × 2,000 = 48,000 |

|

Total |

1,920 |

|

SR2 = 46,080 |

2,000 |

|

ATR= 54,000 |

SR1 = 48,000 |

Others

Standard gang time (SGT) = 40* hours

Actual gang time (AGT) = 40* hours

Idle time [2,000@20%] = 400 hours

Actual yield or output (AY) [2,000 –400] = 1,600

Again,

|

L1 |

= AT × AR |

= 2,000 × 27 |

= $54,000 |

|

L2 |

= AT × SR |

= 2,000 × 24 |

= $48,000 |

|

L3 |

= (AT – IT) × SR |

= (2,000 – 400) × 24 |

= $38,400 |

|

L4 |

= ST × SR |

= 1,920 × 24 |

= $46,080 |

Now,

|

Labour Rate Variance (LRV) |

= L1 – L2 |

= 54,000 – 48,000 |

= 6,000 U |

|

Labour Idle Time Variance (LITV) |

= L2 – L3 |

= 48,000 – 38,400 |

= 9,600 U |

|

Labour Efficiency Variance (LEV) |

= L3 – L4 |

= 38,400 – 46,080 |

= (7,680) F |

|

Labour Cost Variance (LCV) |

= L1 – L4 |

= 54,000 – 46,080 |

= 7,920 U |

By formula method:

Labour rate variance (LRV)

= Actual time × (Standard rate – Actual rate)

= AT × (SR – AR)

= 2,000 × (24 – 27)

= 2,000 × – 3

= $(6,000) U

Labour Idle Time Variance (LITV)

Idle time = 2,000 hours @ 20% = 400 hours

= Idle time × Standard rate

= IT × SR

= 400 hours × $24

= $9,600 U

Labour Efficiency Variance (LEV)

= Standard rate × (Standard time – Actual time)

= SR × (ST – AT)

= 24 × (1,920 – 1,600)

= 24 × 320

= $7,680 F

Labour cost variance (LCV)

= (Standard time × Standard rate) – (Actual time × Actual rate)

= (ST × SR) – (AT × AR)

= (1,920 × 24) – (2,000 × 27)

= 46,080 – 54,000

= $(7,920) U

Keep in Mind (KIM)

|

Idle time variance always unfavourable or adverse for factory. |

|

In efficiency variance, actual time (AT) is taken after deducting idle time. |

(5) Labour mix variance LMV | Gang composition variance, GCV

The difference between standard labour grade and actual labour grade are known as labour mix variance.

There may be difference types of labour in the company.

They are unskilled labour, semi-skilled labour, skilled labour and highly skilled labour etc.

Their mix in the work is known gang composition, labour mix variance or gang composition variance.

There are different rules for labour mix variances.

When standard number of labour and actual number of labour is equal:

LMV = Standard rate × (Revised standard time – Actual time)

Where:

Revised standard time = Standard time × (Actual yield ÷ Standard yield)

When standard number of labour and actual number of labour is not equal:

|

LITV |

= Idle time × Standard rate |

|

|

= IT × SR |

|

|

Or |

|

LMV |

[(Actual mix ÷ Standard mix) × Standard rate of standard mix] – (Standard rate of actual mix) |

|

|

[(ΣAT ÷ ΣST) × SR × ST] – (SR × AT) |

Where:

ST = standard time = Standard labour No. × Standard gang time

AT = actual time = Actual labour No. × Actual gang time

ΣAT = Total of AT = total of Actual labour No. × Actual gang time

ΣST = Total of ST = total of Standard labour No. × Standard gang time

(6) Labour yield variance, LYV | Labour output variance, LOV

The difference between actual output of the workers and standard output of the workers are known as labour yield variance.

It can be also found out by the difference between labour mix variance and labour idle time variance.

When actual mix (number) and standard mix (number) are not vary or difference: (when idle time is not given)

|

LYV |

= Standard cost per unit × (Actual yield or output – Standard yield for actual input) |

|

Or |

= SC × (AY – SY) |

Standard cost

= Standard No. × Standard rate × Standard gang time

= SN × SR × SGT

Standard cost per unit (SC)

= Total standard cost ÷ Standard yield = (SR2 × SGT) ÷ Standard yield = SR3

When actual mix (number) and standard mix (number) are vary or difference: (when idle time is given)

|

LYV |

= Standard cost per unit × (Actual yield or output – Revised standard yield or output) |

|

Or |

= SC × (AY – RSY) |

Revised actual time (RAT)

= Actual Number (Standard gang time – Idle time)

= AN (SGT – IT)

Revised standard yield

= SY × ΣRAT ÷ ΣST

Four (4) variances with mix variance but without ideal time

|

Computation: |

Standard rate per unit (SR1, SR2) |

||

|

L1 = AGT × ATR |

SR1 = standard rate per unit of actual mix |

||

|

L2 = AGT × SR1 |

SR2 = standard rate per unit of standard mix |

||

|

L3 = AGT × SR2 |

|

||

|

L4 = SGT or AY* × SR2 |

|

||

|

|

|||

|

Variances: |

by table |

by formula |

|

|

Labour Rate Variance (LRV) |

= L1 – L2 |

= AT × (SR – AR) |

|

|

Labour Mix Variance (LMV) |

= L2 – L3 |

= [ΣAT ÷ ΣST × SR × ST] – (SR × AT) |

|

|

Labour Efficiency Variance (LEV) |

= L3 – L4 |

= SR (ST – AT) |

|

|

Labour Cost Variance(LCV) |

= L1 – L4 |

= (ST × SR) – (AT × AR) |

|

|

|

|||

|

If actual yield is not given in the question, standard gang time (SGT*) is taken |

|||

Keep in Mind (KIM)

|

If there are different between standard number of workers and actual number of workers, answer of mix variance and yield variance are different in table method and formula method. |

|

Gang composition means labour mix variance. |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 2C

The following data related to labour are given below MN Manufacturing Company:

Standard gang time was 30 hours but actual gang was 32 hours.

|

Standard labour mix |

Actual labour mix |

||||

|

Labour |

No. |

Rate per hour ($) |

Labour |

No. |

Rate per hour ($) |

|

Men |

100 |

60 |

Men |

80 |

65 |

|

Women |

40 |

36 |

Women |

50 |

40 |

|

Boys |

60 |

24 |

Boys |

70 |

20 |

Required: (a) Labour Rate Variance (LRV); (b) Labour Mix Variance (LMV); (c) Labour Efficiency Variance (LEV);

(d) Labour Cost Variance (LCV)

[Answer: LRV = 10,240 U; LMV = 19,200 F; LEV = 1,440 F; LCV = $8,800 U]

SOLUTION:

By table method

Given and working note:

|

Labour |

Standard |

Actual |

Standard × Actual |

||||

|

|

SN |

SR |

Amount |

AN |

AR |

Amount |

SR × AN |

|

Men |

100 |

60 |

6,000 |

80 |

65 |

5,200 |

60 × 80 = 4,800 |

|

Women |

40 |

36 |

1,440 |

50 |

40 |

2,000 |

36 × 50 = 1,800 |

|

Boys |

60 |

24 |

1,440 |

70 |

20 |

1,400 |

24 × 70 = 1,680 |

|

Total |

SR2 = 8,880 |

|

ATR = 8,600 |

SR1 = 8,280 |

|||

Others

Standard gang time (SGT) = 30* hours

Standard output or yield =?

Actual gang time (AGT) = 32 hours

Actual output or yield =?

SR1 = standard rate in actual mix = $8,280

SR2 = standard rate in standard mix = $8,880

Again

|

L1 = AGT × ATR |

= 32 × 8,600 |

= $275,200 |

|

L2 = AGT × SR1 |

= 32 × 8,280 |

= $264,960 |

|

L3 = AGT × SR2 |

= 32 × 8,880 |

= $284,160 |

|

L4 = AY* × SR2 or [SGT × SR2] |

= 30 × 8,880 |

= $266,400 |

Keep in Mind (KIM)

|

If actual yield (AY) is not given, standard gang time (SGT) is taken. |

Now,

|

Labour Rate Variance (LRV) |

= L1 – L2 |

= 275,200 – 264,960 |

= 10,240 U |

|

Labour Mix Variance (LMV) |

= L2 – L3 |

= 264,960 – 284,160 |

= (19,200) F |

|

Labour Efficiency Variance (LEV) |

= L2 – L4 |

= 264,960 – 266,400 |

= (1,440) F |

|

Labour Cost Variance (LCV) |

= L1 – L4 |

= 275,200 – 266,400 |

= 8,800 U |

By formula method:

Given and working note:

|

Labour |

Standard |

Actual |

||||||

|

|

SN |

SR |

SGT |

ST = SN × SGT |

AN |

AR |

AGT |

AT = AN × AGT |

|

Men |

100 |

60 |

30 |

3,000 |

80 |

65 |

32 |

2,560 |

|

Women |

40 |

36 |

30 |

1,200 |

50 |

40 |

32 |

1,600 |

|

Boys |

60 |

24 |

30 |

1,800 |

70 |

20 |

32 |

2,240 |

|

Total |

200 |

|

ΣST = 6,000 |

200 |

|

ΣAT = 6,400 |

||

Labour rate variance (LRV)

|

LRV |

= AT (SR – AR) |

|

|

|

Men |

= 2,560 (60 – 65) |

= 2,560 × – 5 |

= (12,800) U |

|

Women |

= 1,600 (36 – 40) |

= 1,600 × – 4 |

= (6,400) U |

|

Boys |

= 2,240 (24 – 20) |

= 2,240 × 4 |

= 8,960 F |

|

Total |

|

|

= $10,240 U |

Labour mix variance (LMV)

|

LMV |

= [(ΣAT ÷ ΣST) × SR × ST] – (SR × AT) |

|

|

|

Men |

= [(6,400 ÷ 6,000) × 60 × 3,000] – (60 × 2,560) |

= 192,000 – 153,600 |

= 38,400 F |

|

Women |

= [(6,400 ÷ 6,000) × 36 × 1,200] – (36 × 1,600) |

= 46,080 – 57,600 |

= (11,520) U |

|

Boys |

= [(6,400 ÷ 6,000) × 24 × 1,800] – (24 × 2,240) |

= 46,080 – 53,760 |

= (7,680) U |

|

Total |

|

|

= $19,200 F |

Labour Efficiency Variance (LEV)

|

LEV |

= Standard rate × (Standard time – Actual time) |

||

|

|

= SR × (ST – AT) |

|

|

|

Men |

= 60 × (3,000 – 2,560) |

= 60 × 440 |

= 26,400 F |

|

Women |

= 36 × (1,200 – 1,600) |

= 36 × – 400 |

= (14,400) U |

|

Boys |

= 24 × (1,800 – 2,240) |

= 24 × – 440 |

= (10,560) U |

|

Total |

|

|

= $1,440 F |

Labour cost variance (LCV)

|

LCV |

= (Standard time × Standard rate) – (Actual time × Actual rate) |

||

|

|

= (ST × SR) – (AT × AR) |

|

|

|

Men |

= (3,000 × 60) – (2,560 × 65) |

= 180,000 – 166,400 |

= 13,600 F |

|

Women |

= (1,200 × 36) – (1,600 × 40) |

= 43,200 – 64,000 |

= (20,800) U |

|

Boys |

= (1,800 × 24) – (2,240 × 20) |

= 43,200 – 44,800 |

= (1,600) U |

|

Total |

|

|

= $(8,800) U |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 2D

The following data related to labour are given by ABC Small industries:

|

Labour |

Standard labour mix |

Actual labour mix |

|||

|

|

No. |

Rate per hour ($) |

Labour |

No. |

Rate per hour ($) |

|

Grade A |

12 |

22.50 |

Grade A |

15 |

20.00 |

|

Grade B |

8 |

17.50 |

Grade B |

6 |

18.75 |

|

Grade C |

4 |

12.50 |

Grade C |

5 |

10.00 |

Additional information:

In a normal working week of 48 hours, the gang expected to produce 1,200 units. In same working hours, actual output produced 1,000 units due to abnormal idle time of 8 hours.

Required: (a) Labour Rate Variance (LRV); (b) Labour Idle Time Variance (LITV); (c) Labour Mix Variance (LMV);

(d) Labour Yield Variance (LYV); (e) Labour Efficiency Variance (LEV); (f) Labour Cost Variance (LCV)

[Answer: LRV = (2,040) F; LITV = 4,040 U; LMV = (1,800) F;

LYV = Nil; LEV = 5,840 F; LCV = 3,800 U]

SOLUTION:

By table method

Given and working note:

|

Labour |

Standard |

Actual |

Standard × Actual |

||||

|

|

SN |

SR |

Amount |

AN |

AR |

Amount |

SR × AN |

|

Grade A |

12 |

22.50 |

270 |

15 |

20.00 |

300.00 |

22.50 × 15 = 337.50 |

|

Grade B |

8 |

17.50 |

140 |

6 |

18.75 |

112.50 |

17.50 × 6 = 105.00 |

|

Grade C |

4 |

12.50 |

50 |

5 |

10.00 |

50.00 |

12.50 × 5 = 62.50 |

|

Total |

|

|

SR2 = 460 |

|

|

ATR = 462.5 |

SR1 = 505 |

Others

Standard gang time (SGT) = 48 *hours

Standard output per gang?

Standard yield (SY) (given) = 1,200 units

Actual gang time (AGT) = 48* hours

Idle time = 8 hours

Actual yield (AY) (given) = 1,000 units

Note: lack of information, standard gang hours and actual gang hours is same.

SR1 = standard rate in actual mix = $505

SR2 = standard rate in standard mix = $460

SR3 = standard rate in standard output = STG × SR2 ÷ Standard yield = 48 × 460 ÷ 1,200 = $18.4

Again

|

L1 = AGT × ATR |

= 48 × 462.5 |

= $22,200 |

|

L2 = AGT × SR1 |

= 48 × 505 |

= $24,240 |

|

L3 = (AGT – IT) × SR1 |

= (48 – 8) × 505 |

= $20,200 |

|

L4 = (AGT – IT) × SR2 |

= (48 – 8) × 460 |

= $18,400 |

|

L4 = AY × SR3 |

= 1,000 × 18.4 |

= $18,400 |

Now,

|

Labour Rate Variance (LRV) |

= L1 – L2 |

= 22,200 – 24,240 |

= (2,040) F |

|

Labour Idle Time Variance (LITV) |

= L2 – L3 |

= 24,240 – 20,200 |

= 4,040 U |

|

Labour Mix Variance (LMV) |

= L3 – L4 |

= 20,200 – 18,400 |

= 1,800 U |

|

Labour Yield Variance (LYV) |

= L4 – L5 |

= 18,400 – 18,400 |

= Nil (No variance) |

|

Labour Efficiency Variance (LEV) |

= L2 – L5 |

= 24,240 – 18,400 |

= 5,840 U |

|

Labour Cost Variance (LCV) |

= L1 – L5 |

= 22,200 – 18,400 |

= 3,800 U |

By formula method:

Given and working note:

|

Labour |

Standard |

Actual |

||||||

|

|

SN |

SR |

SGT |

ST = SN × SGT |

AN |

AR |

AGT |

AT = AN × AGT |

|

Grade A |

12 |

22.50 |

48 |

576 |

15 |

20.00 |

48 |

720 |

|

Grade B |

8 |

17.50 |

48 |

384 |

6 |

18.75 |

48 |

288 |

|

Grade C |

4 |

12.50 |

48 |

192 |

5 |

10.00 |

48 |

240 |

|

Total |

24 |

|

|

ΣST = 1,152 |

26 |

|

|

ΣAT = 1,248 |

Given and working note:

|

Revised standard time |

= Standard time × Actual yield ÷ Standard yield |

|

|

Grade A |

= 576 × (1,000 ÷ 1,200) |

= 480 hours |

|

Grade B |

= 384 × (1,000 ÷ 1,200) |

= 320 hours |

|

Grade C |

= 192 × (1,000 ÷ 1,200) |

= 160 hours |

|

|

|

= 960 hours |

Labour rate variance (LRV)

|

LRV |

= AT (SR – AR) |

|

|

|

Grade A |

= 720 (22.50 – 20.00) |

= 720 × 2.50 |

= 1,800 F |

|

Grade B |

= 288 (17.50 – 18.75) |

= 288 × – 1.25 |

= (360) U |

|

Grade C |

= 240 (12.50 – 10.00) |

= 240 × 2.50 |

= 600 F |

|

Total |

|

|

= $2,040 F |

Labour Idle Time Variance (LITV)

Given and working note:

Idle time = AN × 8 hours

Grade A = 15 × 8 = 120 hours

Grade B = 6 × 8 = 48 hours

Grade C = 5 × 8 = 40 hours

|

LITV |

= SR × IT |

|

|

Grade A |

= 22.50 × 120 |

= 2,700 U |

|

Grade B |

= 17.50 × 48 |

= 840 U |

|

Grade C |

= 12.50 × 40 |

= 500 U |

|

Total |

|

= $4,040 U |

Labour mix variance (LMV)

|

LMV |

= ΣAT ÷ ΣST × SR × ST – (SR × AT) |

|

|

|

A |

= [1,248 ÷ 1,152 × (22.50 × 576)] – (22.50 × 720) |

= 14,040 – 16,200 |

= (2,160) U |

|

B |

= [1,248 ÷ 1,152 × (17.50 × 384)] – (17.50 × 288) |

= 7,280 – 5,040 |

= 2,240 F |

|

C |

= [1,248 ÷ 1,152 × (12.50 × 192)] – (12.50 × 240) |

= 2,600 – 3,000 |

= (400) U |

|

Total |

|

|

= $(320) U |

Labour Yield Variance (LEV)

= Standard cost per unit (Actual yield – Revised standard yield)

= SC × (AY – RSY)

= 18.40 × (1,000 – 1,080.33)

= 18.40 × –80.33

= (1,533) U

Working note for labour yield variance:

|

Revised actual time |

= AN (SGT – IT) |

|

|

A |

= 15 (48 – 8) |

= 600 |

|

B |

= 6 (48 – 8) |

= 240 |

|

C |

= 5 (48 – 8) |

= 200 |

|

Σ(RAT) |

|

= 1,040 |

Revised standard yield (RSY)

= SY × ƩRAT ÷ ƩST

= 1,200 × 1,040 ÷ 1,152

= 1083.33

Labour Efficiency Variance (LEV)

|

LEV |

= Standard rate × (Standard time – Actual time) |

|

|

|

|

= SR × (RST – AT) |

|

|

|

Grade A |

= 22.50 (480 – 720) |

= 22.50 × –240 |

= (5400) U |

|

Grade B |

= 17.50 (320 – 288) |

= 17.50 × 32 |

= 560 F |

|

Grade C |

= 12.50 (160 – 240) |

= 12.50 × –80 |

= (1,000) U |

|

Total |

|

|

= $(5,840) U |

Labour cost variance (LCV)

|

LCV |

= (Standard time × Standard rate) – (Actual time × Actual rate) |

||

|

|

= (RST × SR) – (AT × AR) |

|

|

|

Grade A |

= (480 × 22.50) – (720 × 20.00) |

= 10,800 – 14,400 |

= (3,600) U |

|

Grade B |

= (320 × 17.50) – (288 × 18.75) |

= 5,600 – 5,400 |

= 200 F |

|

Grade C |

= (160 × 12.50) – (240 × 10.00) |

= 2,000 – 2,400 |

= (400) U |

|

Total |

|

= $(3,800) U |

|

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 2E

The following information is given to you about labour:

|

Standard labour mix |

Actual labour mix |

||||

|

Labour |

No. |

Rate per day ($) |

Labour |

No. |

Rate per day ($) |

|

Trained |

90 |

260 |

Trained |

70 |

265 |

|

Trainee |

40 |

236 |

Trainee |

30 |

240 |

|

Fresher |

50 |

224 |

Fresher |

60 |

220 |

Additional information:

Standard working days were 30 but actual worked days 28 days. Standard output per day of gang time 50 units whereas actual yield 52 units per gang day.

Required: (a) Labour Rate Variance (LRV); (b) Labour Mix Variance (LMV); (c) Labour Yield Variance (LYV);

(d) Labour Efficiency Variance (LEV); (e) Labour Cost Variance (LCV)

[Answer: LRV = 6,440 F; LMV = 148,960 F; LYV = 48,325 U;

LEV = Rs 198,285 U; LCV = $191,845 U]

SOLUTION:

By table method:

|

Labour |

Standard |

Actual |

Standard × Actual |

||||

|

|

SN |

SR |

Amount |

AN |

AR |

Amount |

SR × AN |

|

90 |

260 |

23,400 |

70 |

265 |

18,550 |

260 × 70 = 18,200 |

|

|

Trainee |

40 |

236 |

9,440 |

30 |

240 |

7,200 |

236 × 30 = 7,080 |

|

Fresher |

50 |

224 |

11,200 |

60 |

220 |

13,200 |

224 × 60 = 13,400 |

|

Total |

|

|

SR2 = 44,040 |

|

|

ATR = 38,950 |

SR1 = 38,720 |

Others

|

Standard gang time (SGT) |

30* days |

|

Actual gang time (AGT) |

28 days |

|

Standard output per gang |

50 units |

|

Actual output or yield |

52 units |

|

Standard yield (SY) (30 × 50) |

1,500 units |

|

Actual yield (AY) (28 × 52) |

1,456 units |

Note: lack of information, standard gang hours and actual gang hours is same.

SR1 = standard rate in actual mix = $38,720

SR2 = standard rate in standard mix = $44,040

SR3 = standard rate in standard output = SGT × SR2 ÷ Standard yield = 30 × 44,040 ÷ 1,500 = $880.80

Again

|

L1 = AGT × (ATR) |

= 28 × 38,950 |

= $10,90,600 |

|

L2 = AGT × SR1 |

= 28 × 38,720 |

= $10,84,160 |

|

L3 = AGT × SR2 |

= 28 × 44,040 |

= $12,33,120 |

|

L4 = AY × SR3 |

= 1,456 × 888.8 |

= $12,82,445 |

Now,

|

Labour Rate Variance (LRV) |

= L1 – L2 = 10,90,600 – 10,84,160 |

= 6,440 U |

|

Labour Mix Variance (LMV) |

= L2 – L3 = 10,84,160 – 12,33,120 |

= (148,960) F |

|

Labour Yield Variance (LYV) |

= L3 – L4 = 12,33,120 – 12,82,445 |

= (49,325) F |

|

Labour Efficiency Variance (LEV) |

= L2 – L4 = 10,84,160 – 12,82,445 |

= (198,285) F |

|

Labour Cost Variance (LCV) |

= L1 – L4 = 10,90,600 – 12,82,445 |

= (191,845) F |

By formula method:

Given and working note:

|

Labour |

Standard |

Actual |

||||||

|

|

SN |

SR |

SGT |

ST = SN × SGT |

AN |

AR |

AGT |

AT = AN × AGT |

|

Trained |

90 |

260 |

30 |

2,700 |

70 |

265 |

28 |

1,960 |

|

Trainee |

40 |

236 |

30 |

1,200 |

30 |

240 |

28 |

840 |

|

Fresher |

50 |

224 |

30 |

1,500 |

60 |

220 |

28 |

1,680 |

|

Total |

180 |

|

|

ΣST = 5,400 |

160 |

|

|

ΣAT = 4,480 |

Here, standard yield 1,500 units and actual yields 1,456.

They are different; therefore revised standard time is required.

|

Revised standard time |

= Standard time × Actual labour yield ÷ Standard labour yield |

|

|

Trained |

= 2,700 × (1,456 ÷ 1,500) |

= 2,620.8 |

|

Trainee |

= 1,200 × (1,456 ÷ 1,500) |

= 1,164.8 |

|

Fresher |

= 1,500 × (1,456 ÷ 1,500) |

= 1,456 |

Labour rate variance (LRV)

|

LRV |

= AT (SR – AR) |

|

|

|

Trained |

= 1,960 (260 – 265) |

= 1,960 × – 5 |

= (9,800) U |

|

Trainee |

= 840 (236 – 240) |

= 840 × – 4 |

= (3,360) U |

|

Fresher |

= 1,680 (224 – 220) |

= 1,680 × 4 |

= 6,720 F |

|

Total |

|

|

= $6,440 U |

Labour mix variance (LMV)

|

LMV |

= [(ƩAT ÷ ƩST) SR × ST] – (SR × AT) |

|

|

|

Trained |

= [(4,480 ÷ 5,400) × 260 × 2,700] – (260 × 1,960) |

= 582,400 – 509,600 |

= 72,800 F |

|

Trainee |

= [(4,480 ÷ 5,400) × 236 × 1,200] – (236 × 840) |

= 234,951 – 198,240 |

= 36,709 F |

|

Fresher |

= [(4,480 ÷ 5,400) × 224 × 1,500] – (224 × 1,680) |

= 278,756 – 376,320 |

= (97,564) U |

|

Total |

|

|

= $11,945 F |

Labour Yield Variance (LEV)

= Standard cost per unit × (Actual yield – Standard yield)

= SC × (AY – SY)

= 880.8 × (1,456 – 1,500)

= 880.8 × –44

= (38,755)

Standard cost per unit (SC)

= SR2 × SGT ÷ Standard yield = SR3 = Total standard cost ÷ Standard yield

= 44,040 × 30 ÷ 1,500

= 880.8

Keep in Mind (KIM)

|

Answer is different between table method and formula method because standard number of workers (SN) and actual number of workers (AN) are different. |

Labour Efficiency Variance (LEV)

|

LEV |

= Standard rate × (Revised standard time – Actual time) |

||

|

|

= SR × (RST – AT) |

|

|

|

Trained |

= 260 × (2620.8 – 1,960) |

= 260 × 660.8 |

= 171,808 F |

|

Trainee |

= 236 × (1,164.8 – 840) |

= 236 × 324.8 |

= 76,653 F |

|

Fresher |

= 224 × (1,456 – 1,680) |

= 224 × – 224 |

= (50,176) U |

|

Total |

|

|

= $198,285 F |

Labour cost variance (LCV)

|

LCV |

= (Revised standard time × Standard rate) – (Actual time × Actual rate) |

||

|

|

= (RST × SR) – (AT × AR) |

|

|

|

Trained |

= (2,620.8 × 260) – (1,960 × 265) |

= 681,408 – 519,400 |

= 162,008 F |

|

Trainee |

= (1,164.8 × 236) – (840 × 240) |

= 274,893 – 201,600 |

= 73,293 F |

|

Fresher |

= (1,456 × 224) – (1,680 × 220) |

= 326,144 – 369,600 |

= (43,456) U |

|

Total |

|

|

= $191,845 F |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 2F

The following information available:

|

Standard |

Actual |

||||

|

Labour |

No. |

Rate per hour ($) |

Labour |

No. |

Rate per hour ($) |

|

Grade A |

30 |

24 |

Grade A |

40 |

21.0 |

|

Grade B |

15 |

18 |

Grade B |

10 |

19.5 |

|

Grade C |

10 |

12 |

Grade C |

5 |

9.0 |

Normal working hours in week is 40 hours.

It is expected to produce by gang 2,000 hours during period. Actual yield was 1,980 hours due to 4 abnormal idle times.

Required: (1) Labour rate variance; (2) Labour ideal time variance; (3) Labour mix variance; (4) Labour yield variance

(5) Labour efficiency variance; (6) Labour cost variance

[Answer: LRV = (4,800) F; LITV = 4,800 U; LMV = 3,240 U;

LYV = (3,999) F; LEV = (4,044) F; LCV = (756) F]

SOLUTION:

Given and working note:

|

Labour Grade |

Standard |

Actual |

Standard × Actual |

||||

|

|

SN |

SR |

Amount |

AN |

AR |

Amount |

SR × AN |

|

Grade A |

30 |

24 |

720 |

40 |

21.0 |

840 |

24 × 40 = 960 |

|

Grade B |

15 |

18 |

270 |

10 |

19.5 |

195 |

18 × 10 = 180 |

|

Grade C |

10 |

12 |

120 |

5 |

9.0 |

45 |

12 × 5 = 60 |

|

Total |

|

SR2 = 1,110 |

|

|

ATR = 1,080 |

SR1 = 1,200 |

|

Others

|

Standard gang time (SGT) |

40* hours |

|

Idle time |

4 DLH |

|

Standard yield (SY) (given) |

2,000 units |

|

Actual gang time (AGT) |

40* hours |

|

|

|

|

Actual output or yield |

1,980 |

Note: lack of information, standard gang hours and actual gang hours is same.

SR1 = standard rate in actual mix = $1,200

SR2 = standard rate in standard mix = $1,110

SR3 = standard rate in standard output = SGT × SR2 ÷ Standard yield = 40 × 1,100 ÷ 2,000 = $22.20

Again,

|

L1 |

= AGT × ATR |

= 40 × 1,080 |

= 43,200 |

|

L2 |

= AGT × SR1 |

= 40 × 1,200 |

= 48,000 |

|

L3 |

= (AGT – IT) × SR1 |

= (40 –4) × 1,200 |

= 43,200 |

|

L4 |

= (AGT – IT) × SR2 |

= (40 –4) × 1,110 |

= 39,960 |

|

L5 |

= AY × SR3 |

= 1,980 × 22.20 |

= 43,956 |

Now,

|

Labour Rate Variance (LRV) |

= L1 – L2 |

= 43,200 – 48,000 |

= (4,800) F |

|

Labour Ideal Time Variance (LITV) |

= L2 – L3 |

= 48,000 – 43,200 |

= 4,800 U |

|

Labour Mix Variance (LMV) |

= L3 – L4 |

= 43,200 – 39,960 |

= 3,240 U |

|

Labour Yield Variance (LEV) |

= L4 – L5 |

= 39,960 – 43,956 |

= (3,996) F |

|

Labour Efficiency Variance (LEV) |

= L2 – L5 |

= 48,000 – 43,956 |

= (4,044) F |

|

Labour Cost Variance (LCV) |

= L1 – L5 |

= 43,200 – 43,956 |

= (756) F |

By formula method:

Given and working note:

|

Labour |

Standard |

Actual |

||||||

|

|

SN |

SR |

SGT |

ST = SN × SGT |

AN |

AR |

AGT |

AT = AN × AGT |

|

Grade A |

30 |

24 |

40 |

1,200 |

40 |

21.00 |

40 |

1,600 |

|

Grade B |

15 |

18 |

40 |

600 |

10 |

19.50 |

40 |

400 |

|

Grade C |

10 |

12 |

40 |

400 |

5 |

9.00 |

40 |

200 |

|

Total |

55 |

|

|

ΣST = 2,200 |

55 |

|

|

ΣAT = 2,200 |

Here, standard yield 2,000 units and actual yield 1,980.

They are different; therefore revised standard time is required.

|

Revised standard time |

= Standard time × Actual yield ÷ Standard yield |

|

|

Grade A |

= 1,200 × (1,980 ÷ 2,000) |

= 1,188 |

|

Grade B |

= 600 × (1,980 ÷ 2,000) |

= 594 |

|

Grade C |

= 400 × (1,980 ÷ 2,000) |

= 396 |

Labour rate variance (LRV)

|

(LRV) |

= AT (SR – AR) |

||

|

Grade A |

= 1,600 (24 – 21) |

= 1,600 × 3 |

= 4,800 F |

|

Grade B |

= 400 (18 – 19.5) |

= 400 × –1.5 |

= (600) U |

|

Grade C |

= 200 (12 – 9) |

= 200 × 3 |

= 600 F |

|

Total |

|

|

= 4,800 F |

Labour ideal time variance (LITV)

|

LITV |

= SR × IT |

|

|

Grade A |

= 24 × 160 |

= 3840 U |

|

Grade B |

= 18 × 40 |

= 720 U |

|

Grade C |

= 12 × 20 |

= 240 U |

|

Total |

|

$4,800 U |

Working note:

|

Idle time |

= Actual No. of worker × Idle time per worker |

|

|

Grade A |

= 40 × 4 |

= 160 |

|

Grade B |

= 10 × 4 |

= 40 |

|

Grade C |

= 5 × 4 |

= 20 |

Labour Mix Variance (LMV)

|

LMV |

= [ΣAT ÷ ΣST × SR × ST] – (SR × AT) |

||

|

Grade A |

= [2,200 ÷ 2,200 × (24 × 1,200)] – (24 × 1,600) |

= 28,800 – 38,400 |

= (9,600) U |

|

Grade B |

= [2,200 ÷ 2,200 × (18 × 600)] – (18 × 400) |

= 10,800 – 7,200 |

= 3,600 F |

|

Grade C |

= [2,200 ÷ 2,200 × (12 × 400)] – (12 × 200) |

= 4,800 – 2,400 |

= 2,400 F |

|

Total |

|

|

= $(3,600) U |

Labour Yield Variance (LEV)

= Standard cost per unit (Actual yield – Revised standard yield)

= SC (AY – RSY)

= 22.20 (1,980 – 1,800)

= 22.20 × 180

= 3,996 F

Working note for labour yield variance:

|

Standard cost |

= SN × SR × SGT |

|

|

Grade A |

= 30 × 24 × 40 |

= 28,800 |

|

Grade B |

= 15 × 18 × 40 |

= 10,800 |

|

Grade C |

= 10 × 12 × 40 |

= 4,800 |

|

Total |

|

= $44,400 |

Standard cost per unit (SC)

= Total standard cost ÷ Standard yield

= $44,400 ÷ 2,000 units

= $22.20

Revised actual time (RAT)

|

RAT |

= AN (SGT – IT) |

|

|

A |

= 40 (40 – 4) |

= 1,440 |

|

B |

= 10 (40 – 4) |

= 360 |

|

C |

= 5 (40 – 4) |

= 180 |

|

Σ(RAT) |

|

= 1,980 |

Revised standard yield (RSY)

= SY × ƩRAT ÷ ƩST

= 2,000 × 1980 ÷ 2,200

= 1,800

Labour Efficiency Variance (LEV)

|

LEV |

= Standard rate × (Revised standard time – Actual time) |

||

|

|

= SR × (RST – AT) |

||

|

Grade A |

= 24 (1,188 – 1,600) |

= 24 × –412 |

= (9,888) U |

|

Grade B |

= 18 (594 – 400) |

= 18 × 194 |

= 3,492 F |

|

Grade C |

= 12 (396 – 200) |

= 12 × 196 |

= 2,352 F |

|

Total |

|

|

= $4,044 U |

Labour cost variance (LCV)

|

LCV |

= (Revised standard time × Standard rate) – (Actual time × Actual rate) |

||

|

|

= (RST × SR) – (AT × AR) |

||

|

Trained |

= (1,188 × 24) – (1,600 × 21) |

= 28,512 – 33,600 |

= (5,088) |

|

Trainee |

= (594 × 18) – (400 × 19.5) |

= 10,692 – 7,800 |

= 2,892 F |

|

Fresher |

= (396 × 12) – (200 × 9) |

= 4,752 – 1,800 |

= 2,952 F |

|

Total |

|

|

= $756 F |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 2G

GM Manufacturing Company has following data:

|

Standard |

Actual |

||||||

|

Labour |

No./mix |

Rate ($) |

Cost |

Labour |

No./mix |

Rate ($) |

Cost |

|

Skilled |

32 |

30 |

960 |

Skilled |

28 |

40 |

1,120 |

|

Semi-skilled |

12 |

20 |

240 |

Semi-skilled |

18 |

30 |

540 |

|

Unskilled |

6 |

10 |

60 |

Unskilled |

4 |

20 |

80 |

|

Total |

50 |

|

1,260 |

Total |

50 |

|

1,740 |

|

Standard output 1,800 units |

Actual worked hours during a week 40 |

||||||

|

Standard gang time (STG)? |

|

||||||

Required: (Direct)

(1) Labour rate variance; (2) Labour mix variance; (3) Labour efficiency variance; (4) Labour cost variances

[Answer: LRV = Rs 20,000 U; LMV = Rs (800) F;

LEV = Rs 4,240 U; LCV = Rs 24,240 U]

SOLUTION

|

Labour |

Standard |

Actual |

Standard × Actual |

||||

|

|

SN |

SR |

SN × SR |

AN |

AR |

AN × AR |

Std Rate × Actual No. |

|

Skilled |

32 |

30 |

960 |

28 |

40 |

1120 |

30 × 28 = 840 |

|

Semi-skilled |

12 |

20 |

240 |

18 |

30 |

540 |

20 × 18 = 360 |

|

Unskilled |

6 |

10 |

60 |

4 |

20 |

80 |

10 × 4 = 40 |

|

Total |

SN = 50 |

|

SR2 = 1260 |

|

|

ARN =1740 |

SR1 = 1,240 |

Other

Standard yield (SY) = 1800

Standard gang time (STG) = SY ÷ SN = 1,800 ÷ 50 = 36

Actual gang time (AGT) = 40 hours

Actual yield/output (AY) = Nil

SR1 = standard rate in actual mix = $1,240

SR2 = standard rate in standard mix = $1,260

Again

|

L1 |

= AGT × (AN × AR) |

= 40 × 1740 |

= $69,600 |

|

L2 |

= AGT × SR1 |

= 40 × 1240 |

= $49,600 |

|

L3 |

= AGT × SR2 |

= 40 × 1260 |

= $50,400 |

|

L4 |

= SGT × SR2 |

= 36 × 1260 |

= $45,360 |

Now,

|

Labour Rate Variance (LRV) |

= L1 – L2 |

= 69,600 – 49,600 |

= 20,000 U |

|

Labour Mix Variance (LMV) |

= L2 – L3 |

= 49,600 – 50,400 |

= – 800 F |

|

Labour Efficiency Variance (LEV) |

= L2 – L4 |

= 49,600 – 45,360 |

= 4,240 U |

|

Labour Cost Variance (LCV) |

= L1 – L4 |

= 69,600 – 45,360 |

= 24,240 U |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 2H

The following information is given to you about labour by XYZ Manufacturing Company:

|

Standard labour mix |

Actual labour mix |

||||

|

Labour |

No. |

Rate per hour ($) |

Labour |

No. |

Rate per hour ($) |

|

Grade A |

10 |

18.75 |

Grade A |

13 |

18.00 |

|

Grade B |

5 |

12.00 |

Grade B |

4 |

12.75 |

|

Grade C |

5 |

10.50 |

Grade C |

3 |

9.75 |

Normal working hours in a week 40 hours and expected to produced 1,000 units.

2 hours lost due to abnormal idle time and 960 units were produced.

Required: (a) Labour rate variance; (b) Labour ideal time variance; (c) Labour mix variance; (d) Labour yield variance;

(e) Labour efficiency variance; (f) Labour cost variance

[Answer: LRV = (360) F; LITV = 646.50 U; LMV = (930) F;

LYV = (120) F; LEV = (1,330) F; LCV = (1,440)]

SOLUTION:

By formula method:

Given and working note:

|

Labour |

Standard |

Actual |

||||||

|

|

SN |

SR |

SGT |

ST = SN × SGT |

AN |

AR |

AGT |

AT = AN × AGT |

|

Grade A |

10 |

18.75 |

40 |

400 |

13 |

18.00 |

40 |

520 |

|

Grade B |

5 |

12.00 |

40 |

200 |

4 |

12.75 |

40 |

160 |

|

Grade C |

5 |

10.50 |

40 |

200 |

3 |

9.75 |

40 |

120 |

|

Total |

20 |

|

|

ΣST = 800 |

20 |

|

|

ΣAT = 800 |

Here, standard yield 1,000 units and actual yields 960.

They are different; therefore revised standard time is required.

Revised standard time (RST)

|

RST |

= Standard time × Actual yield ÷ Standard yield |

|

|

Grade A |

= 400 × (960 ÷ 1,000) |

= 384 |

|

Grade B |

= 200 × (960 ÷ 1,000) |

= 192 |

|

Grade C |

= 200 × (960 ÷ 1,000) |

= 192 |

|

Total hours |

|

= 768 |

Labour rate variance (LRV)

|

LRV |

= AT (SR – AR) |

||

|

Grade A |

= 520 (18.75 –18.00) |

= 520 × 0.75 |

= 390 F |

|

Grade B |

= 160 (12.00 – 12.75) |

= 160 × – 0.75 |

= (120) U |

|

Grade C |

= 120 (10.50 – 9.75) |

= 120 × 0.75 |

= 90 F |

|

Total |

|

|

= 360 F |

Labour Idle Time Variance (LITV)

Given and working note:

|

Idle time |

= AN × 2 hours |

|

|

Grade A |

= 13 × 2 |

= 26 hours |

|

Grade B |

= 4 × 2 |

= 8 hours |

|

Grade C |

= 3 × 2 |

= 6 hours |

Again,

|

LITV |

= SR × IT |

|

|

Grade A |

= 18.75 × 26 |

= 487.50 U |

|

Grade B |

= 12.00 × 8 |

= 96 U |

|

Grade C |

= 10.50 × 6 |

= 63 U |

|

Total |

|

= 646.50 U |

Labour mix variance (LMV)

|

LMV |

= ƩAT ÷ ƩST × SR × ST – (SR × AT) |

||

|

Grade A |

= [(800 ÷ 800) × 18.75 × 400] – (18.75 × 520) |

= 7,500 – 9,750 |

= (2250) U |

|

Grade B |

= [(800 ÷ 800) × 12.00 × 200] – (12.00 × 160) |

= 2,400 – 1,920 |

= 480 F |

|

Grade C |

= [(800 ÷ 800) × 10.50 × 200] – (10.50 × 120) |

= 2,100 – 1,260 |

= 840 F |

|

Total |

|

|

= (930) U |

Labour Yield Variance (LEV)

= Standard cost per unit × (Actual yield – Revised standard yield)

= SC × (AY – RSY)

= 12 × (960 – 950)

= 12 × 10

= 120 F

Working note for labour yield variance:

|

Standard cost |

= SN × SR × SGT |

|

|

Grade A |

= 10 × 18.75 × 40 |

= 7,500 |

|

Grade B |

= 5 × 12.00 × 40 |

= 2,400 |

|

Grade C |

= 5 × 10.50 × 40 |

= 2,100 |

|

Total |

|

$12,000 |

Standard cost per unit (SC)

= Total standard cost ÷ Standard yield

= $12,000 ÷ 1,000 units

= $12

Revised actual time

|

RAT |

= AN (SGT – IT) |

|

|

A |

= 13 (40 –2) |

= 494 |

|

B |

= 4 (40 –2) |

= 152 |

|

C |

= 3 (40 –2) |

= 114 |

|

ΣRAT |

|

= 760 |

Revised standard yield (RSY)

= SY × ƩRAT ÷ ƩST

= 1,000 × 760 ÷ 800

= 950

Labour Efficiency Variance (LEV)

|

LEV |

= Standard rate × (Revised standard time – Actual time) |

||

|

|

= SR × (RST – AT) |

||

|

Grade A |

= 18.75 (384 – 520) |

= 18.75 × –136 |

= (2,550) U |

|

Grade B |

= 10.00 (192 – 160) |

= 10.00 × 32 |

= 320 F |

|

Grade C |

= 12.50 (192 – 120) |

= 12.50 × 72 |

= 900 F |

|

Total |

|

|

= (1,330) U |

Labour cost variance (LCV)

|

LCV |

= (Revised standard time × Standard rate) – (Actual time × Actual rate) |

||

|

|

= (RST × SR) – (AT × AR) |

||

|

Grade A |

= (384 × 18.75) – (520 × 18.00) |

= 7,200 – 9,360 |

= (2,160) U |

|

Grade B |

= (192 × 10.00) – (160 × 12.75) |

= 1,920 – 2,040 |

= (120) U |

|

Grade C |

= (192 × 12.50) – (160 × 9.75) |

= 2,400 – 1,560 |

= 840 F |

|

Total |

|

|

= (1,440) U |

Here, Amount = Rs = $ = £ = € = ₹ = Af = ৳ = Nu = Rf = රු = Br = P = Birr = Currency of your country

PROBLEM: 2I

|

Standard: |

||

|

Raw materials |

Composition |

Rate |

|

A |

40% |

$5 |

|

B |

60% |

$4 |

Standard loss in blending is 10%

An article is produced by blending two raw materials:

The company produced 1,000 articles out of the following details during March:

|

Raw materials |

Stock (kg) March 1 |

Stock (kg) March 31 |

Purchases (kg) |

During March ($) |

|

A |

60 |

30 |

570 |

3,135 |

|

B |

40 |

50 |

910 |

3,185 |

Find out: (a) Material price variance; (b) Materials usage variance; (c) Material mix variance; (d) Materials yield variance

[Answer: (nearest) MPV = Rs (150) F; MUV = Rs 1,700 U;

MMV= Nil; MYV= Rs 1,700 U;

* Production = Opening stock + Purchase – Closing stock;